Market Insights — Week of March 20, 2026

A Shifting Rate Environment, Rising Uncertainty

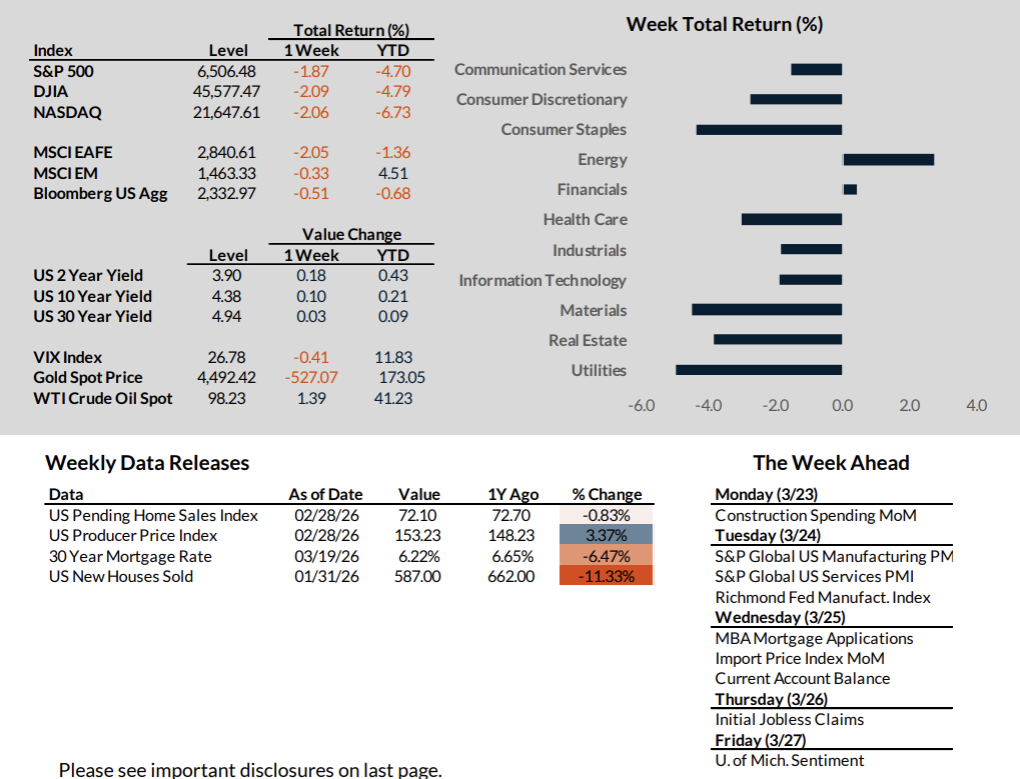

Markets moved lower this week as inflation concerns resurfaced and geopolitical tensions continued to evolve.

- The S&P 500 declined 1.87%, with broad weakness across sectors

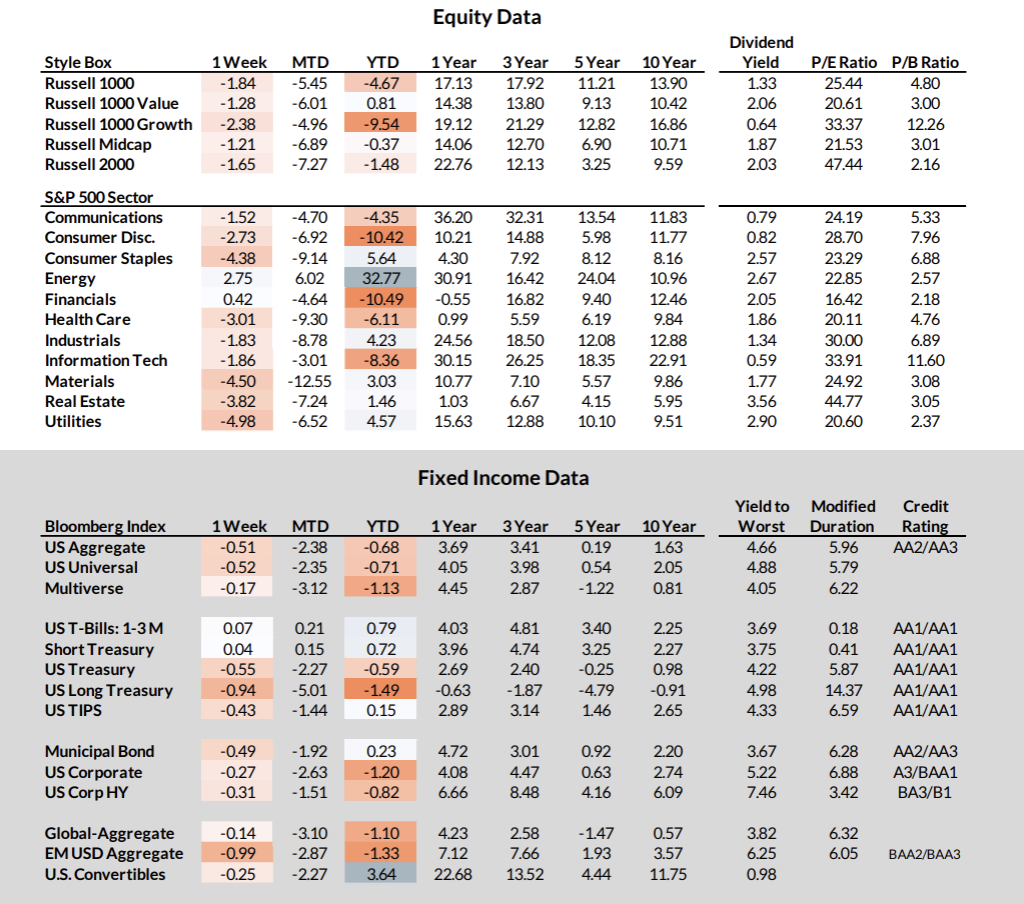

- Treasury yields moved higher, with the 10-year closing near 4.38%

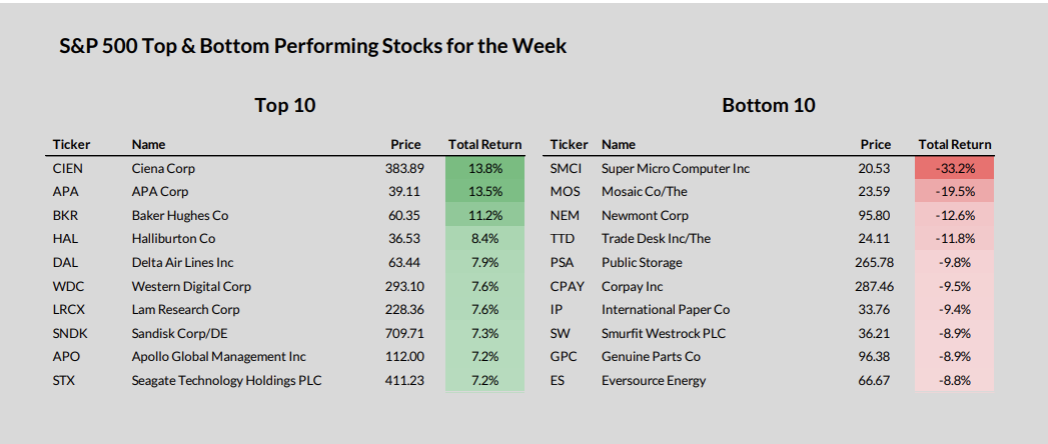

- Energy was the only sector to post gains, supported by rising oil prices

- Overseas markets followed a similar pattern, with most major indices finishing lower

At a high level, the story remains consistent:

Inflation pressures are proving more persistent than expected, and markets are adjusting to a higher-for-longer rate environment.

What We’re Watching

1. The Fed’s Position Is Becoming More Restrictive Than Expected

While the Federal Reserve held rates steady, updated projections suggest fewer rate cuts ahead than markets previously anticipated.

- Inflation expectations were revised higher

- Several policymakers now expect no rate cuts this year

- The threshold for easing policy has increased

This signals a shift from “when will rates fall” to “how long will they remain elevated.”

2. Geopolitical Risk Is Being Repriced Quickly

Escalation in the Middle East is beginning to impact multiple asset classes:

- Oil prices have moved higher, reinforcing inflation concerns

- Equity markets have declined for multiple consecutive weeks

- Recession probabilities have increased meaningfully in a short period

Markets are now attempting to price in both inflation risk and economic slowdown simultaneously—a more complex environment than earlier in the year.

3. Market Signals Suggest Liquidity Pressure Beneath the Surface

One of the more notable developments this week was a sharp decline in gold prices despite rising uncertainty.

- Gold experienced its steepest weekly drop in decades

- Treasury yields continued to rise

- Commodities broadly showed signs of stress

This type of divergence can sometimes indicate liquidity-driven selling rather than purely fundamental shifts.

What This Means in a Retirement Context

While short-term market movements can feel disconnected from long-term planning, environments like this tend to influence decision timing more than investment selection.

When rates remain elevated and inflation expectations shift:

- Income opportunities may improve—but require more deliberate positioning

- Tax planning windows (such as Roth conversion opportunities) can compress or shift

- Portfolio withdrawal sequencing becomes more sensitive to timing

- Waiting for “more clarity” can quietly reduce flexibility over time

This is where coordination becomes increasingly important.

Not because markets are unpredictable—but because multiple variables are moving at once.

The Bigger Picture

This is not an unusual market environment—but it is a more constrained one.

- Inflation is no longer clearly declining

- Rate cuts are no longer clearly imminent

- Geopolitical risks are no longer isolated

In periods like this, the focus often shifts away from performance and toward positioning and optionality.

Closing Perspective

Markets will continue to adjust as new information becomes available.

What tends to matter more over time is not reacting to each shift—but understanding how these conditions influence:

- income decisions

- tax exposure

- and long-term flexibility

That’s where most outcomes are ultimately shaped.