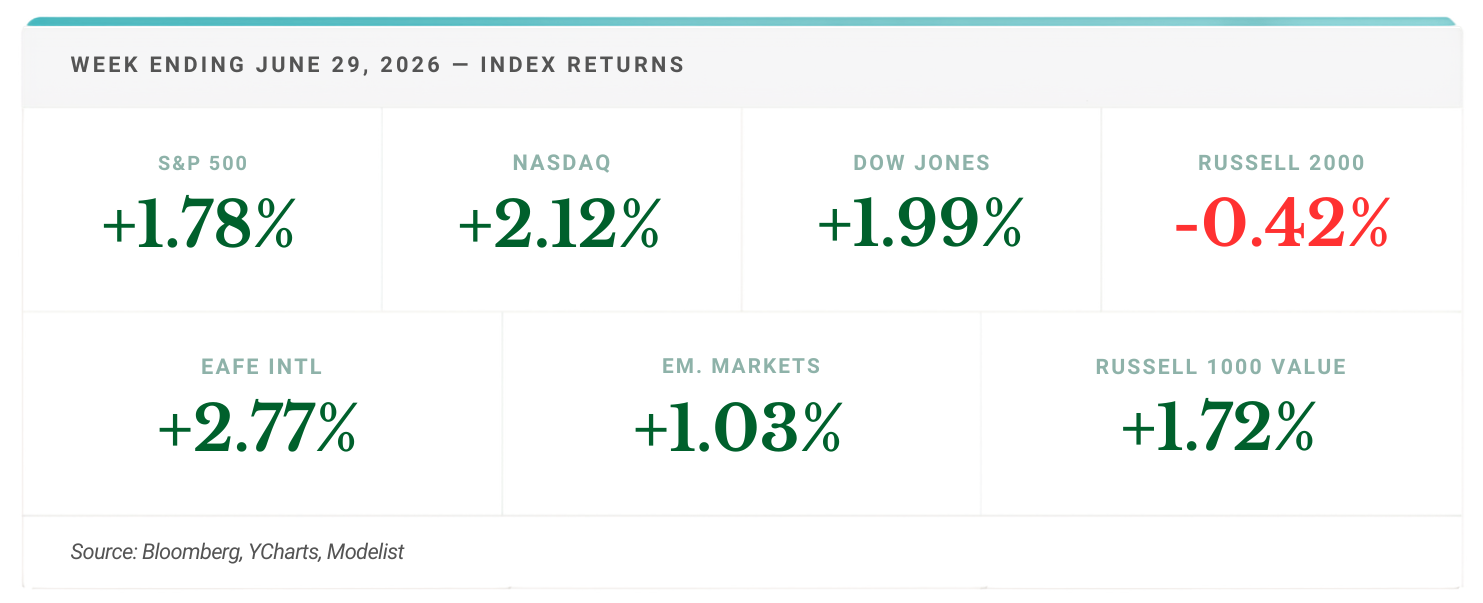

The Bond Market Repriced Your Income Last Week. The Stock Market Got the Headlines.

The index closed higher, but utilities and real estate led the market lower. The Treasury market explains why, and it matters more to retirement income than the headline does.