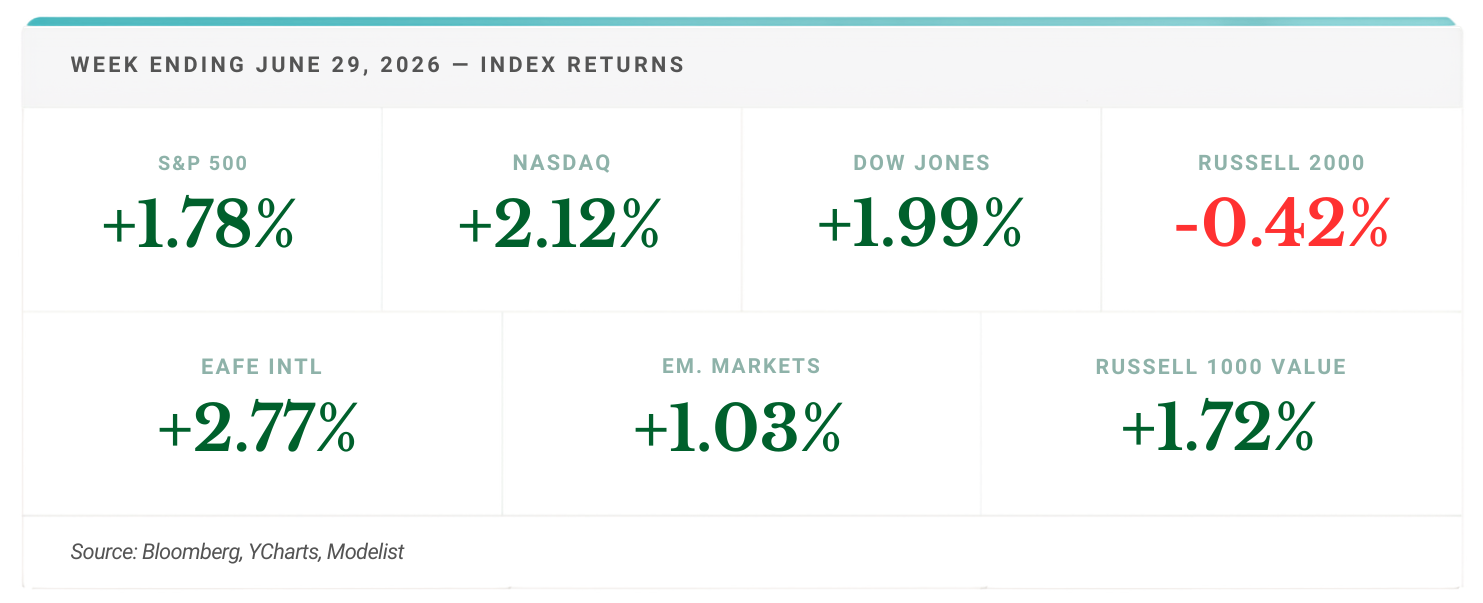

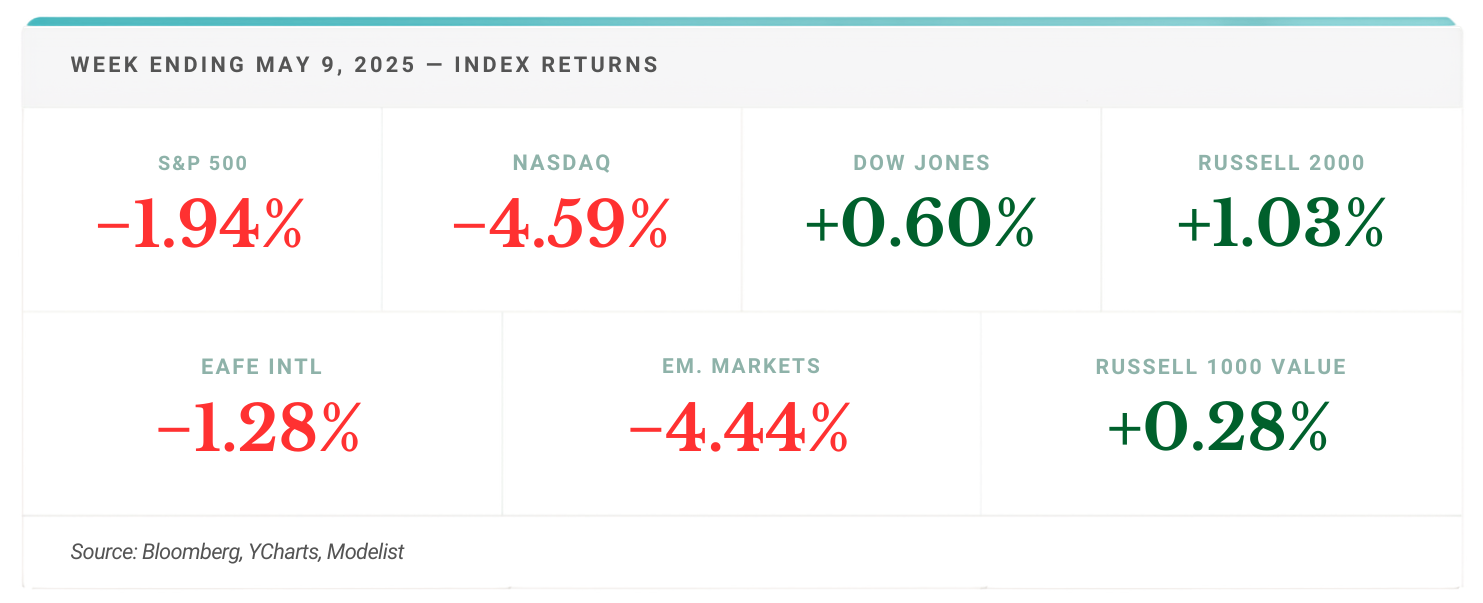

A Week Ago, Falling Yields Said Inflation Was Cooling. This Week They Reversed — and the Fed Meets Wednesday.

Stocks slipped, but the real move was in the bond market: yields jumped and oil hit $89 as the market repriced inflation — two days before the Fed. What it means for a retirement portfolio.