Inflation Raises the Stakes — Markets Split as Hot Data Dims the Rate-Cut Clock

The week's story wasn't really about stock prices. It was about what's sitting underneath them: an inflation picture that is still running hotter than the Fed wants, and the quiet but significant shift that creates for anyone drawing income from a portfolio in retirement.

The Week in Markets

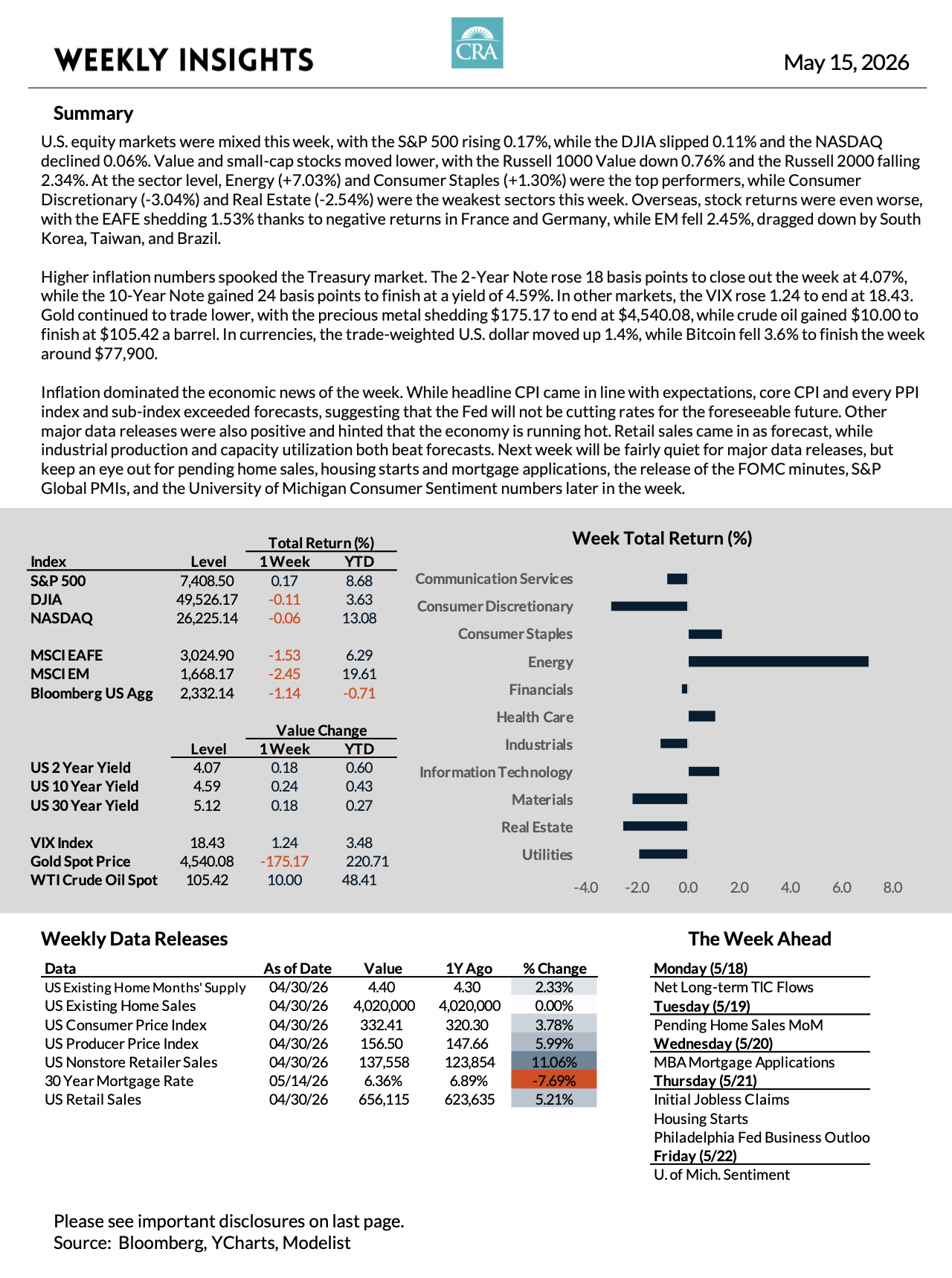

U.S. equities ended the week mixed, with the S&P 500 barely holding positive ground, up 0.17%, while the Dow slipped 0.11% and the NASDAQ edged down 0.06%. The real action was at the edges. Small-cap stocks bore the brunt of the inflation repricing, with the Russell 2000 falling 2.34% and the Russell 1000 Value declining 0.76% — two segments that tend to feel rate pressure more acutely than large-cap growth.

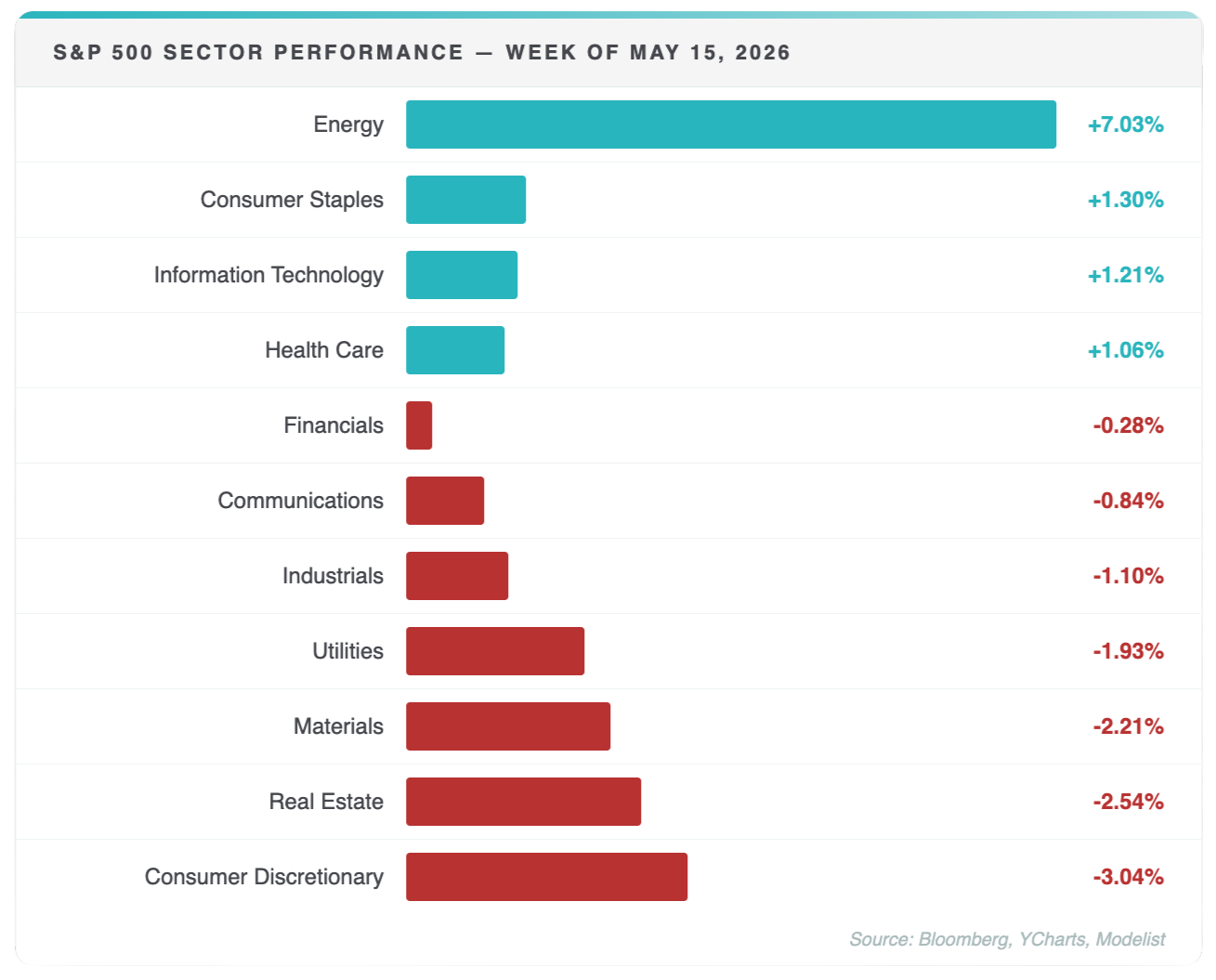

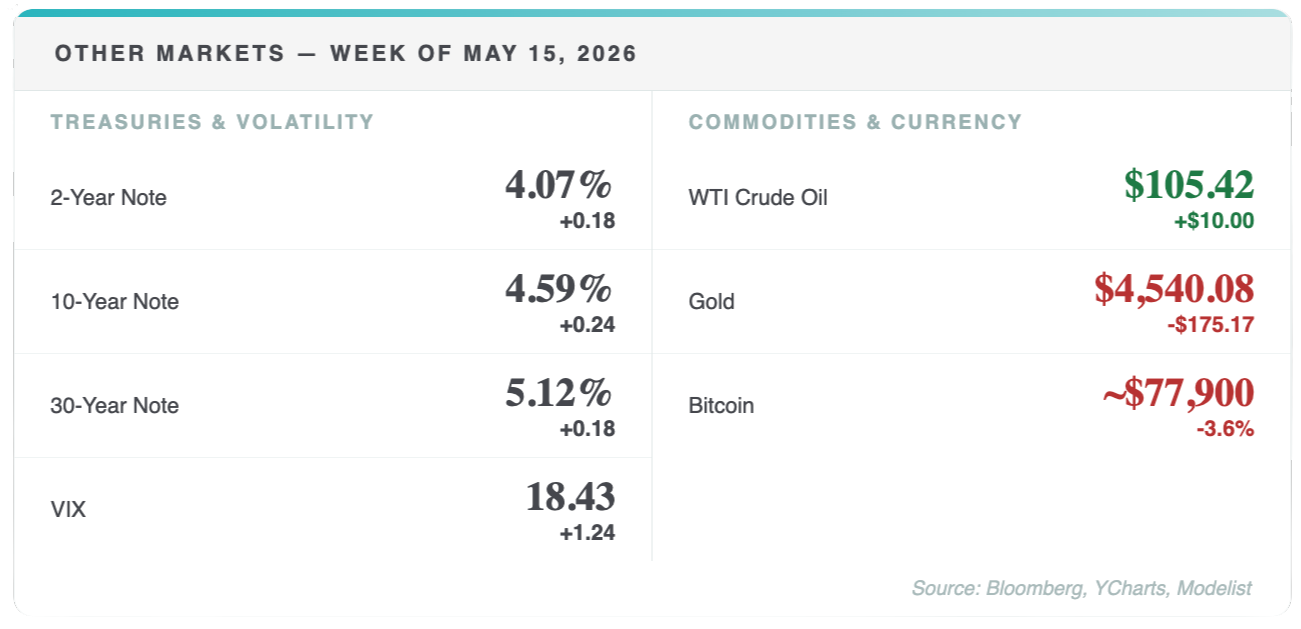

At the sector level, Energy surged 7.03% as crude oil climbed $10.00 to $105.42 a barrel, and Consumer Staples added 1.30%. Everything else largely gave ground. Consumer Discretionary fell 3.04%, Real Estate dropped 2.54%, and Utilities declined 1.93% — a reminder that when yields move, rate-sensitive sectors feel it quickly. Overseas markets had a rougher week: the MSCI EAFE lost 1.53%, dragged by weakness in France and Germany, while Emerging Markets fell 2.45%, led lower by South Korea, Taiwan, and Brazil.

Things We're Watching

Inflation Is Still in Charge

Headline CPI came in as expected, but core CPI and every PPI index and sub-index exceeded forecasts. That pattern matters. When only headline comes in hot, it is often energy or food — categories that tend to reverse. When core CPI and PPI are both running above expectations, it suggests inflation has more staying power in the pipeline. For now, the Fed has little room to move, and the longer rates stay elevated, the more that affects the math for retirees who depend on their portfolio to generate income. The question worth watching: does this stay confined to energy and supply chains, or does it begin spreading into services, wages, and consumer expectations?

The Treasury Market Is Repricing

The 2-Year Note rose 18 basis points to 4.07%, and the 10-Year Note jumped 24 basis points to close at 4.59%. That is a meaningful move in a single week. For retirees with existing bond holdings or bond funds, rising yields mean falling prices on paper — and for those in the income distribution phase, it also narrows the window for refinancing, restructuring, or rebalancing without taking real losses. The 30-Year yield now sits at 5.12%. Sequence risk, often discussed in the context of equities, applies to bonds too when the shift happens quickly.

AI Is Still Carrying the Earnings Story — But the Load Is Getting Heavier

The S&P 500 held up because a handful of AI-linked and technology names continued to perform. Cisco gained 22.4% on the week. Palo Alto Networks rose 16.8%. The mega-cap earnings narrative remains strong enough to offset the macro pressure — for now. But as oil prices climb, yields rise, and the rate-cut timeline extends, the weight being carried by that earnings story grows heavier. Valuation support increasingly depends on earnings revisions staying strong enough to absorb the rate environment. That is not a reason for alarm, but it is a reason to understand how concentrated the market's resilience actually is.

Want the Full Picture?

The full Modelist Market Insights report includes multi-period equity and fixed income data, sector detail tables, and style box performance. It is the data behind this commentary.

View Full Weekly Market Report →

What This Means for Your Retirement Plan

This is exactly the kind of week that the CRAve Life Advisory Process™ is built for. Not because anything broke — nothing did. But because weeks like this are where fragmented plans quietly absorb damage that coordinated ones can often avoid. Rising yields affect bond holdings, income strategies, and Roth conversion math differently depending on how a plan is structured. If your income, your tax strategy, and your investment positioning are working together, a week like this is something your advisor is already accounting for. That is what coordinated planning is supposed to provide: not a prediction, but a structure that holds up when conditions shift.

If you do not have that kind of coordination in place — if your investments, tax planning, and income strategy are being managed separately, or not being reviewed together at all — this is a useful moment to ask whether that changes anything. The 20-Minute Due-Diligence Q&A Call is a no-pressure way to find out how a coordinated approach might apply to your specific situation. You can schedule one by clicking the link below.

Schedule a 20-Minute Due-Diligence Q&A Call →