Retirement: Fighting the Inflation Battle

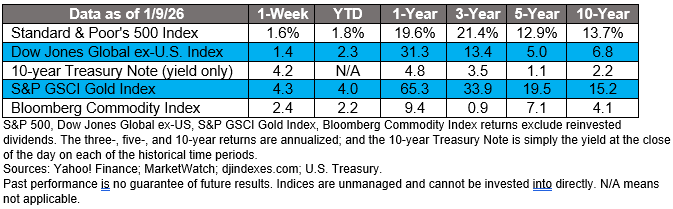

The Markets

A change in leadership.

Last week, investors were presented with a stew of economic and policy developments. These included the surprising announcement that the United States would “run” Venezuela, disappointing jobs data, signs of improved consumer optimism, and a flurry of new policy proposals. Investors weighed what it all means for financial markets, and stocks moved higher.

Here’s what happened:

Geopolitical tensions heightened. “The arrest and indictment of former Venezuela leader Nicolás Maduro roiled energy markets and raised the specter of military interventions in other parts of the world, including Greenland, a territory controlled by NATO ally Denmark,” reported Martin Baccardax of Barron’s.

U.S. jobs growth was soft. 2025 was a tough year to find a job. In December, about 50,000 new jobs were added. That was roughly in line with the monthly average for 2025. In total, about 584,000 jobs were created last year, making it “the worst year for hiring since 2020, when the Covid-19 pandemic resulted in an annual loss,” reported Megan Leonhardt of Barron’s.

Consumer optimism improved. The University of Michigan Consumer Sentiment Index showed that optimism ticked higher. “Improvements in January were seen among lower-income consumers, while sentiment fell for those with higher incomes. All told, while consumers perceived some modest improvement in the economy over the past two months, their sentiment remains nearly 25 [percent] below last January’s reading,” wrote Surveys of Consumers Director Joanne Hsu.

The President proposed new policies. On social media, President Trump proposed a slew of new policies that would:

- Prohibit investment groups from buying single-family homes. In recent years, private equity and other groups have invested heavily in housing, lifting demand and housing prices. After the post, stocks of home builders fell to their lowest level in three years, according to John Authers of Bloomberg.

- Have the government buy $200 billion in mortgage bonds. The intent is to make housing more affordable by having government housing entities Fannie Mae and Freddie Mac purchase mortgage bonds. Analysts had mixed opinions about whether the purchases would push mortgage rates lower, reported Josh Wingrove, Scott Carpenter, and Katy O'Donnell of Bloomberg. Mortgage bonds and home lender stocks rallied.

- Require defense firms to prioritize reinvestment. He indicated the firms should “end stock buybacks, stop issuing dividends and cap executive pay until they invest more in factories and research,” reported Phil Serafino of Bloomberg. After the post stocks of defense companies fell.

- Increase defense spending from $1 trillion to $1.5 trillion dollars in 2027. “The U.S. government is the largest customer of many defense contractors, but it doesn’t have an equity stake or a golden share that can dictate board-level policies. The executive order references the Defense Production Act, a 1950s law, which authorizes the government to compel companies to prioritize its orders over commercial concerns during national emergencies,” reported Al Root of Barron’s. The stocks of defense companies recovered some lost ground after the post, reported the Associated Press.

By the end of the week, market leadership appeared to be changing, as investors leaned into smaller companies and value stocks. “So far this year, areas like materials and industrials are far outpacing tech names. And small-caps are doing the best of all,” reported Avi Salzman of Barron’s.

At the end of the week, market major U.S. stock indexes were higher. The yield on the benchmark 10-year U.S. Treasury finished the week near where it started it.

Retirement: Fighting the Inflation Battle

We’ve all heard stories about how much – or how little – our parents and grandparents paid for their first car or their first home. In 1960s, a brand-new Oldsmobile cost less than $3,000, and the average U.S. home price was $17,800.

Rising prices – a phenomenon called inflation – are a significant risk to retirement. That’s why it’s critical to save as much as you can and invest it to keep pace with or beat inflation over time. In recent years, legislation has made it possible for American workers to boost the amount of money they’re saving in tax-advantaged workplace retirement plans, including:

- 401(k) plans, which are for private-sector workers,

- 403(b) plans, which are for public-sector and non-profit workers, and

- 457(b) plans, which are for government workers.

Catch-up contributions allow people to save more than the maximum plan contribution of $24,500 in 2026. There are four types of catch-up contributions:

- Age 50 catch-up contributions. Participants in 401(k), 403(b), or 457(b) plans can save an additional $8,000 in 2026, as long as they will be age 50 or older by the end of the year.

- Age 60 to 63 catch-up contributions. Participants in 401(k), 403(b), or 457(b) plans, who will be between the ages of 60 and 63 by the end of 2026, can save an additional $11,250 in 2026.

- Fifteen-year catch-up contributions. People who participate in a 403(b) plan and have completed 15 years of service with their organizations can contribute a higher amount to their plans annually, regardless of age. The lifetime limit for these catch-up contributions is $15,000.

- Three-year catch-up contributions. People who save in a 457(b) plan can defer up to twice the annual contribution limit during the three years before normal retirement age (as established by the plan). The amount of the catch-up contribution depends on amounts previously saved in the plan.

In general, one type of catch-up contribution cannot be combined with another type of catch-up contribution. You must choose which to make.

If you have questions about your workplace retirement plan, please get in touch. Just as important, if you don’t have a workplace retirement plan and would like to begin saving for retirement, please contact us. There are other tax-advantaged ways to save for retirement.

Weekly Inspiration

“The true amount [of oil] recoverable in Venezuela today…is closer to 40bn barrels than the 300bn often suggested. And a lot of the untapped oil, deemed ‘extra heavy’, is hard, costly and polluting to extract. To be bankable, Venezuela’s biggest new projects need Brent, the global price benchmark, at $80 a barrel. This year Brent is forecast to fall towards $50. When you are pitching to America’s oil giants, a risk-averse bunch, that’s not a good start. And Venezuela, which confiscated many of their assets in 2007 without compensating them for the trouble, has other problems. It lacks the type of sound legal system, stable politics and functioning economy that foreign companies like to see before opening their wallets.”

― Matthieu Favas, The Economist, January 8, 2026

Best Regards,

California Retirement Advisors