The AI Trade Is Back in Charge — and Friday's Jobs Report Will Decide If It Holds

Tech led. Rates fell. And now the market is waiting on the most important number of the week.

The Week in Markets

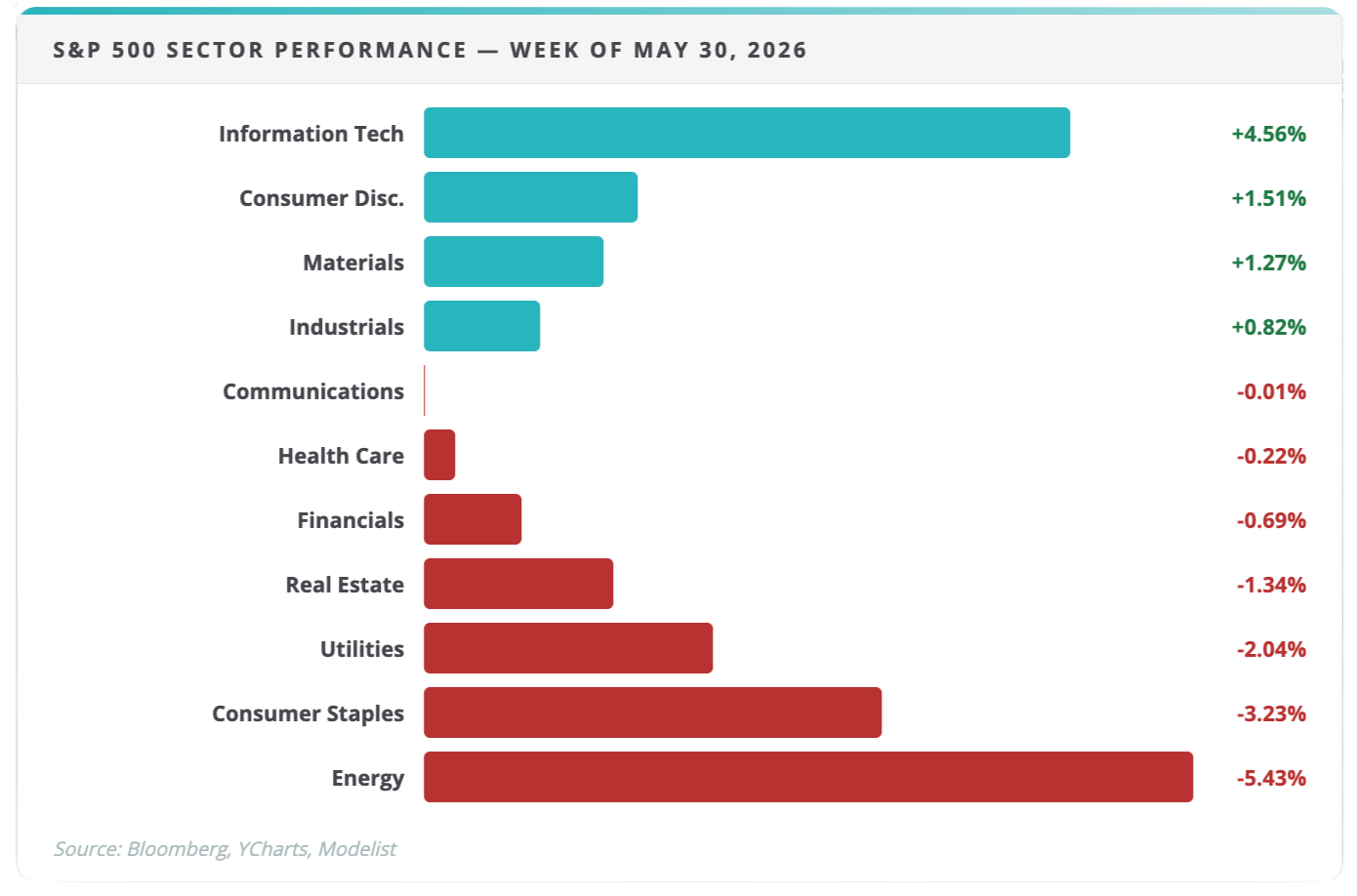

U.S. equity markets moved broadly higher last week, with the NASDAQ leading the major indexes at +2.39%, the S&P 500 gaining 1.44%, and the Dow rising 0.91%. The rotation that defined the prior week — small caps and value stocks taking the wheel — partially reversed, as Information Technology (+4.56%) and Consumer Discretionary (+1.51%) reclaimed leadership. That said, value and small caps still participated: the Russell 1000 Value rose 0.73% and the Russell 2000 gained 1.77%, suggesting the breadth seen in prior weeks hasn't fully unwound.

Energy was the week's clear laggard, falling 5.43%, after news broke that the U.S. and Iran were close to a formal ceasefire agreement. Consumer Staples also declined 3.23%, Utilities fell 2.04%, and Real Estate dropped 1.34%. On the other side, Materials gained 1.27% and Industrials rose 0.82%. Overseas, the MSCI EAFE gained 1.08% behind solid performances in Spain, France, and Japan, while Emerging Markets surged 3.96% — driven by semiconductor-heavy Taiwan and South Korea.

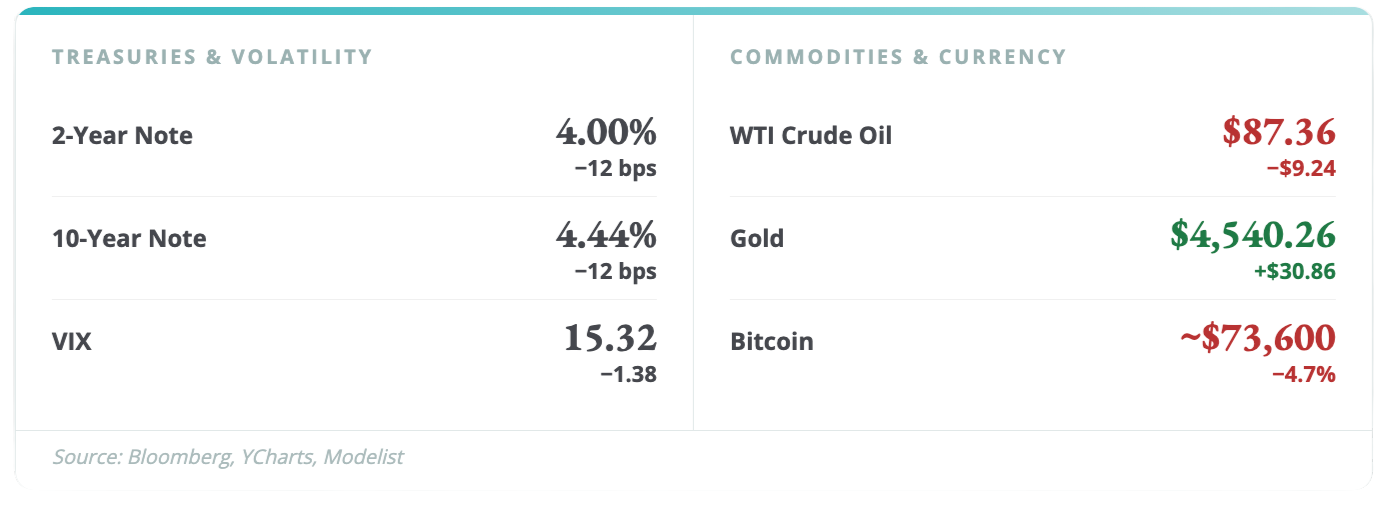

In fixed income, yields fell across the curve, with both the 2-year Note and 10-year Note shedding 12 basis points, finishing at 4.00% and 4.44% respectively. The VIX dropped another 1.38 points to close at 15.32 — still calm. Gold ticked higher to $4,540 an ounce, crude oil fell sharply to $87.36 on the Iran ceasefire headline, and Bitcoin slipped 4.7% to close near $73,600.

Things We're Watching

1. Tech Is Back — and the Concentration Question Returns With It

Last week's breadth story was real. This week, it got complicated. A single sector — Information Technology, up 4.56% — drove a disproportionate share of the market's gains, while defensives and energy sold off hard. That's not necessarily a problem if the underlying earnings thesis holds, but it does mean the rally's durability is once again tied to a short list of names. Global leadership is splintering in an interesting way: emerging markets had a strong week, but Korea and Taiwan — AI and semiconductor plays — led the charge, while China lagged despite improving industrial data. The market is increasingly separating export-driven tech beneficiaries from economies with less reliable domestic demand. That split matters for how portfolios are positioned heading into the second half of the year.

2. The PCE Came In — and It Was Mixed

The week's most anticipated data release arrived Thursday: the PCE report, the Fed's preferred inflation gauge. The headline was mixed. Personal income came in below expectations, but both core and headline inflation measures printed below forecasts — a modest but genuine relief for a market that had been bracing for a hotter number. Q1 GDP was also revised lower, confirming that first-quarter growth was softer than originally reported. On the other side of the ledger, Conference Board Consumer Confidence and Durable Goods Orders both surprised to the upside. The net read: an economy that's neither falling apart nor running hot enough to force the Fed's hand. That's the kind of data environment that keeps policy uncertainty in place — rates stay elevated, timelines stay fuzzy, and markets keep repricing week to week.

3. Friday's Jobs Report Is the Number That Changes Everything

This week's calendar is front-loaded with market-moving data: ISM and S&P Manufacturing and Services PMIs, Construction Spending, and Factory Orders are all due. But the week belongs to Friday's Nonfarm Payrolls and Unemployment Report. In an environment where the market has already priced in a prolonged pause from the Fed, a strong jobs print would reinforce that timeline — and potentially push yields back up. A weaker-than-expected number opens the door for a different conversation. For income-focused retirees, Friday's report is the one data point most likely to move the needle on the rate environment that governs bond yields, CD rates, and the mechanics of withdrawal sequencing.

Want the Full Picture?

The full Market Insights report includes multi-period equity and fixed income data, sector detail tables, style box performance, and the complete economic calendar for the week ahead.

View Full Weekly Market Report →

What This Means for Your Retirement Plan

Tech's resurgence and falling yields last week were genuinely welcome. But the week ahead — with manufacturing data, services data, and Friday's jobs report all landing in rapid succession — means the macro picture is about to get updated again.

For clients of CRA, that's noise, not signal. Your income strategy isn't built around a single jobs print. Your Roth conversion math doesn't hinge on whether yields move 10 basis points in either direction this week. The CRAve Life Advisory Process™ is designed for exactly this: weeks where the data is pulling in multiple directions at once, and where reacting to headlines would almost certainly produce worse outcomes than holding to a coordinated plan.

For those not yet working with a structured approach, Friday's jobs report is a useful lens. Do you know what a strong print means for your bond holdings? What a weak print means for your income floor? If the answer involves checking your brokerage account and hoping for the best, the 20-Minute Due-Diligence Q&A Call is where a better answer starts.

Schedule a 20-Minute Due-Diligence Q&A Call →