The Jobs Report Missed Badly. The Market Hit a Record High. Here's What That Tells You.

The U.S. economy added 57,000 jobs in June — the weakest report since February, with two prior months revised down. The Dow closed the week at a record high. Both of those are true, and understanding why is the key to reading this market right now.

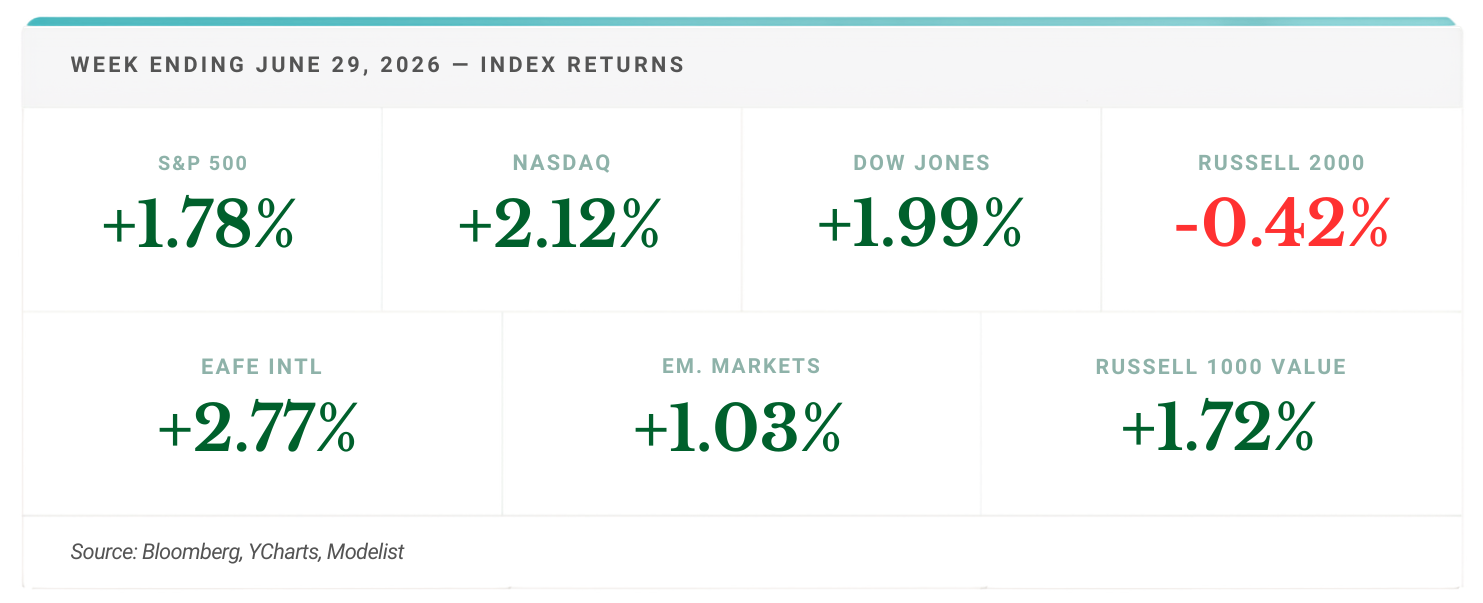

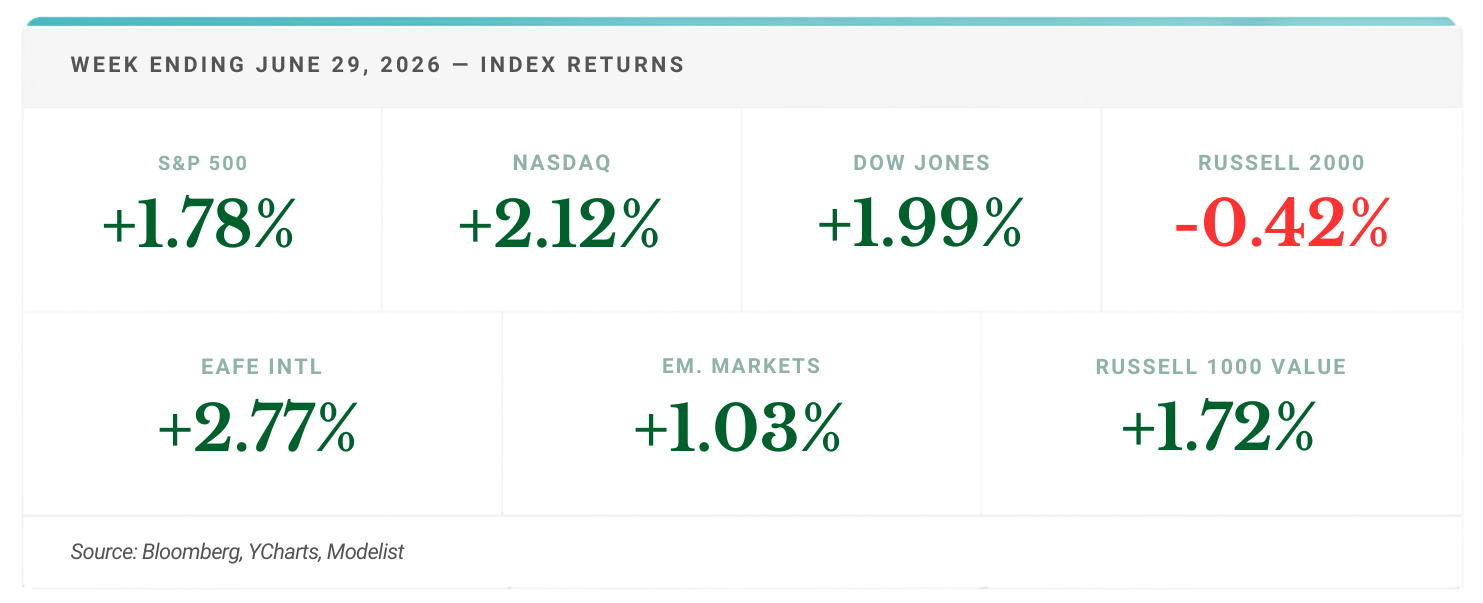

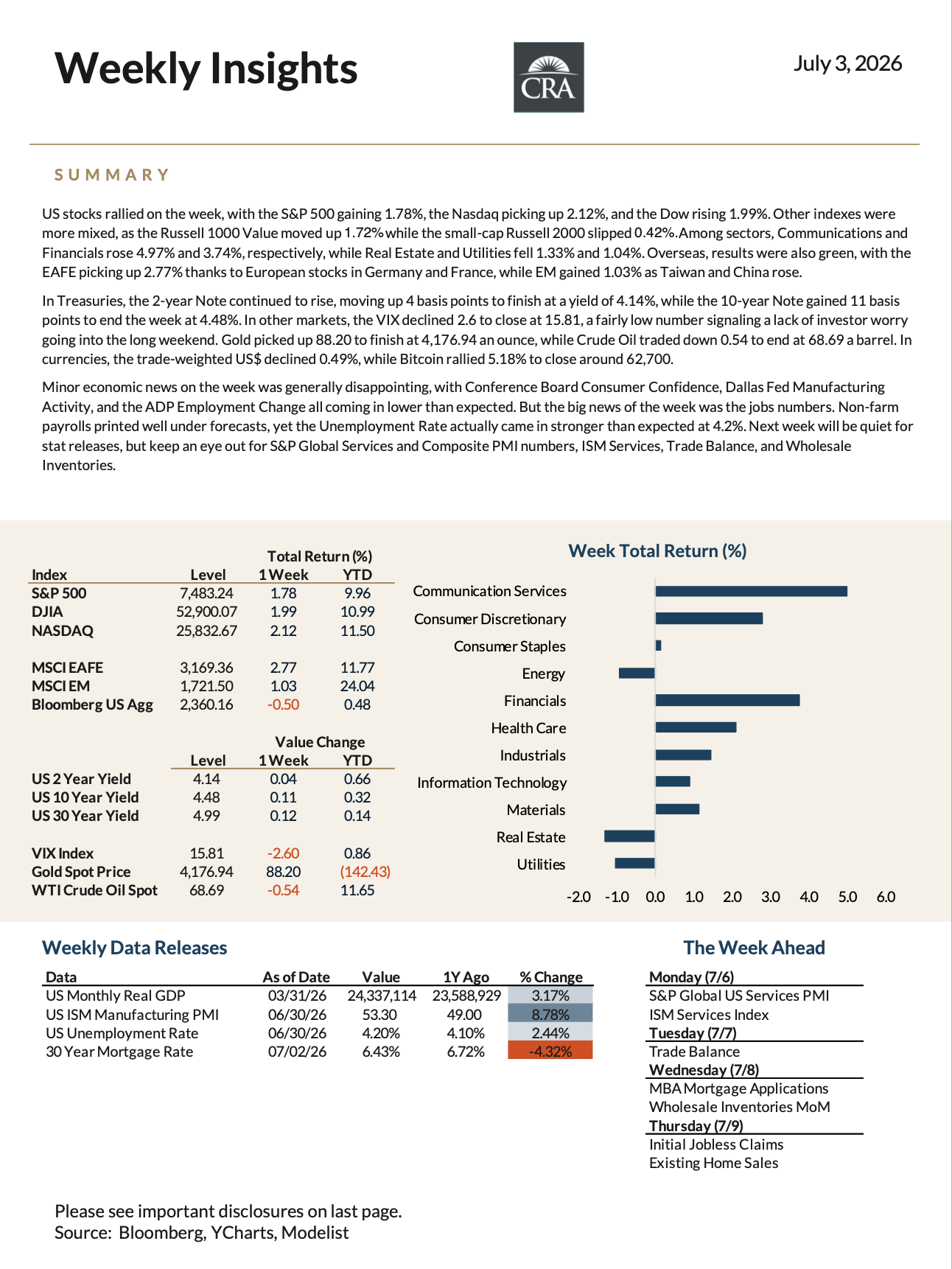

By the old rules, a jobs miss that size sends stocks lower. Instead, the Dow finished the holiday-shortened week up 1.99% at a record, the S&P 500 gained 1.78%, and the Nasdaq added 2.12%.

Good News and Bad News Have Switched Places

For most of the past two decades, investors wanted strong economic data and feared weakness. That logic has inverted. With inflation still elevated, the question hanging over this market isn't when the Fed cuts — it's whether the Fed hikes again. Going into Thursday, futures markets still priced real odds of a July rate increase. After the soft payroll number, those odds fell sharply. A cooling labor market, in this environment, reads as relief: it takes pressure off the Fed without yet signaling real economic damage. Unemployment actually ticked down to 4.2%. The caveat sits on the other side — too much cooling would shift the conversation from inflation relief to growth risk — which is why the pace of the slowdown, not just its direction, is what matters from here.

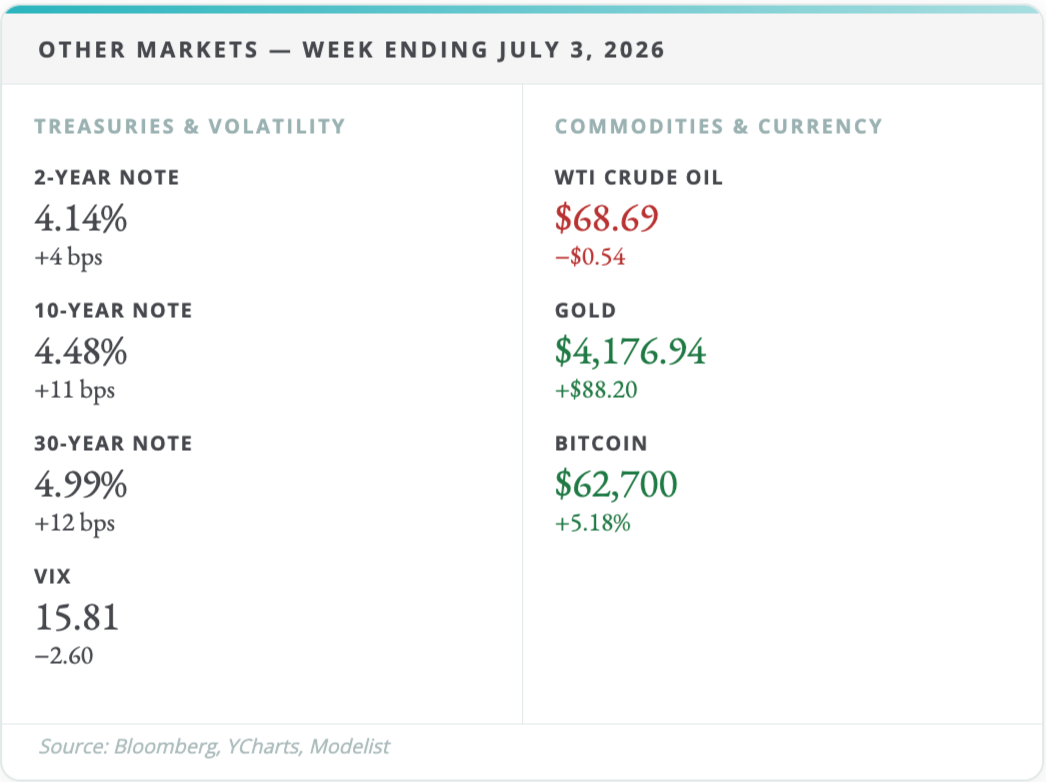

The market's read was calm. Treasury yields ended the week only modestly higher — the 2-year up 4 basis points to 4.14%, the 10-year up 11 to 4.48% — a drift, not a repricing. And the VIX fell 2.6 points to close at 15.81, a low reading for a week that ended with a jobs miss. Yields steady, volatility falling, stocks at records: that's what relief looks like.

The Record High Has a Rotation Underneath It

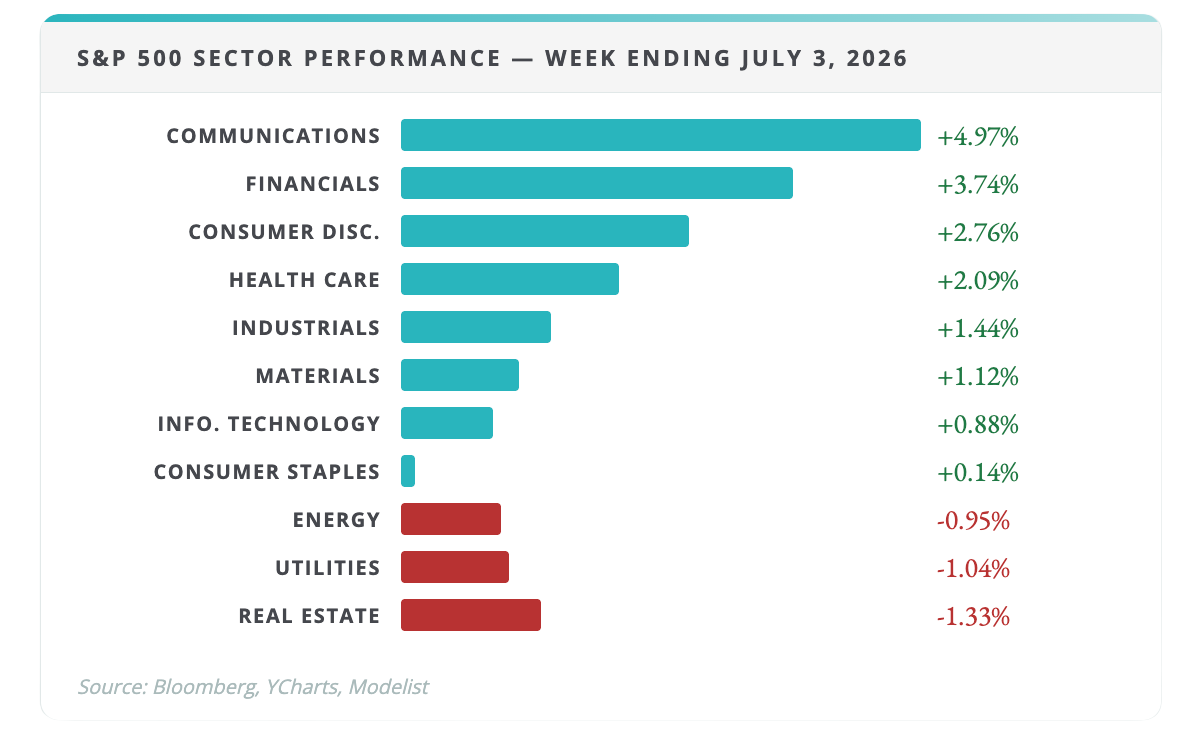

Here's what the headline number hides: the week's gains didn't come from the names that led the first half. The S&P 500's worst performers were concentrated in semiconductor and AI-hardware stocks, several down double digits, as investors questioned whether infrastructure spending has run ahead of the earnings that must eventually justify it. But the selloff was surgical, not sectoral. Information Technology still finished the week up 0.88%, while Communication Services led every sector at +4.97% and Financials added 3.74%. Small caps sat the week out — the Russell 2000 slipped 0.42% — and the breadth extended overseas, with the EAFE gaining 2.77% on European strength. The money leaving the crowded trade didn't leave the market. It moved toward large, established businesses with more ordinary valuations. A record built on broadening participation is structurally healthier than one carried by a single trade. But it sets up the next test.

Earnings Season Is Where This Gets Settled

Q2 earnings season opens in the coming weeks, and expectations — especially for the AI complex — are demanding after the first half's run. The market just demonstrated it will reprice crowded trades quickly when confidence wavers. Companies now have to prove that revenue and margins can justify what investors already paid for them. This week's economic calendar is quiet — ISM Services and trade balance are the highlights — which leaves earnings as the next real catalyst. Between soft-but-not-broken jobs data and a Fed with less reason to move, earnings become the variable that decides whether this rotation is a healthy handoff or the start of something choppier.

Want the Full Picture?

For the complete index returns, all 11 sector breakdowns, treasury yields, and commodities data, view the full report below.

View Full Weekly Market Report →

What This Means for Your Retirement Plan

The inversion is the lesson this week: the same jobs number that would have hurt portfolios in one environment helped them in this one, and no one managing their own retirement should be expected to recalibrate that logic in real time. That's what a coordinated plan is for. The Bucket Plan® doesn't ask you to know whether the next soft data point is relief or warning — near-term income is already insulated from the answer, and the long-term bucket has the time to let earnings season sort out which companies deserve their valuations. Last week rewarded investors who didn't react to the scary headline. Most weeks do.

If Thursday's report — or the selloff in the AI names — raised a question about whether your income plan depends on any of this resolving a particular way, that's exactly the kind of specific question worth twenty minutes.

Schedule a 20-Minute Due-Diligence Q&A Call →