The Market Made Three Assumptions. This Week Grades All of Them.

Stocks shrugged off a broken ceasefire, bonds priced in a hawkish Fed, and a handful of technology names carried the index — all in the same five days. Each of those moves rests on an assumption, and the coming week puts every one of them to the test.

The Week in Markets

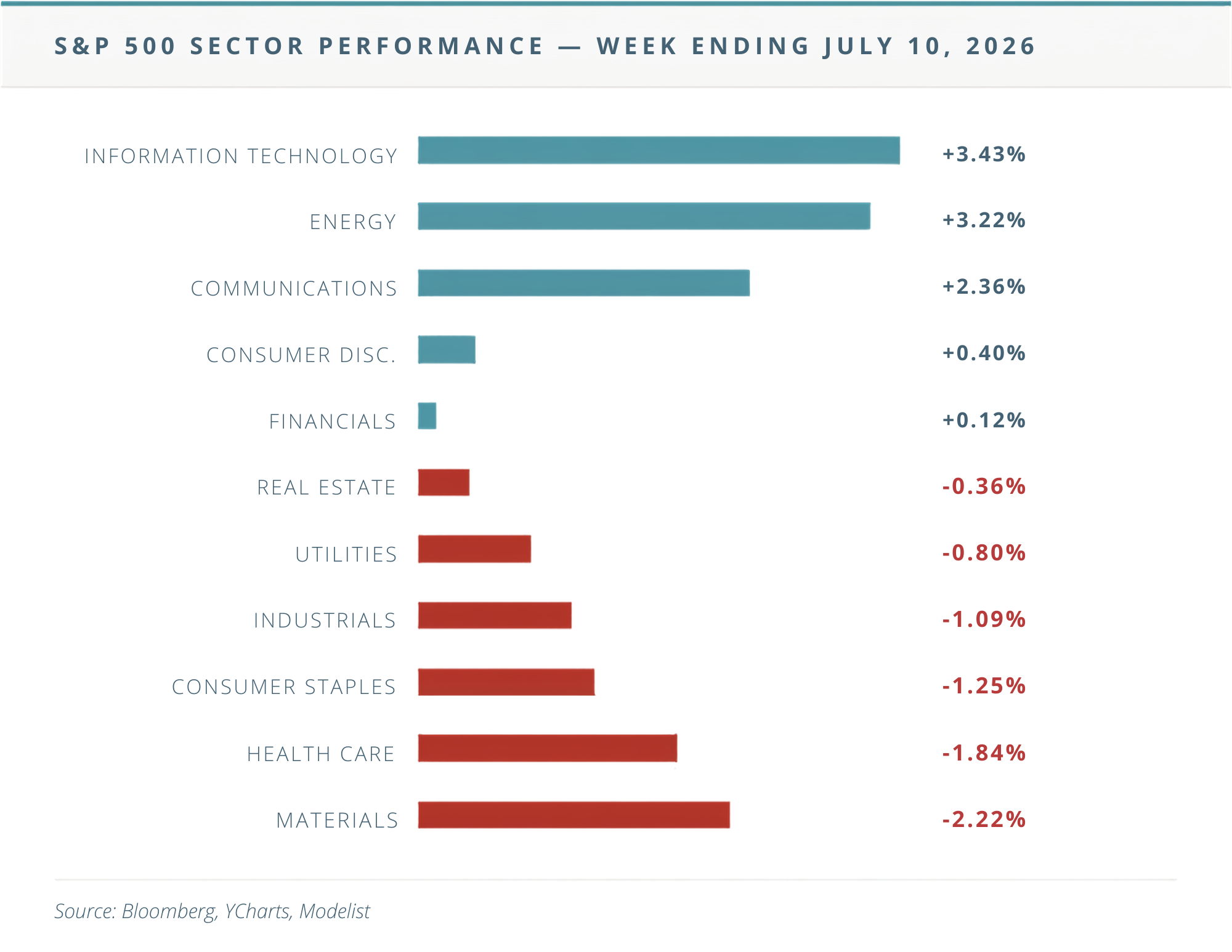

The headline numbers say "quiet week." The S&P 500 added 1.26% to close at 7,575, the Nasdaq rose 1.74%, and the Dow slipped 0.48%. Underneath, the week was anything but quiet — it was narrow. Information Technology (+3.43%) and Energy (+3.22%) did nearly all the lifting, while Materials (-2.22%) and Health Care (-1.84%) sold off. Small caps lagged again, with the Russell 2000 down 0.60%, and international markets fell outright — developed markets (EAFE) shed 1.36% and emerging markets lost 1.73%.

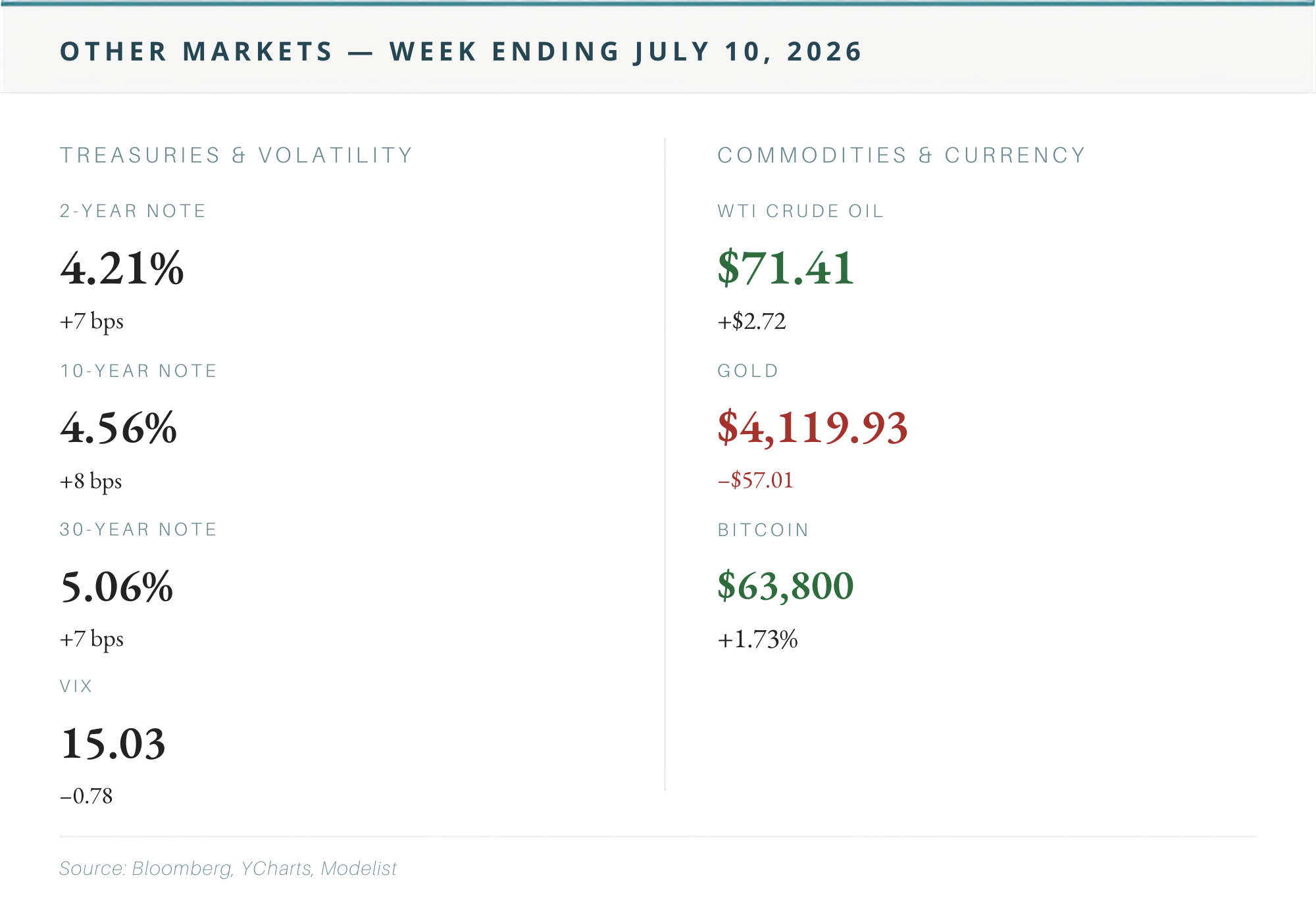

The most telling number of the week wasn't a stock index. The White House declared the Iran ceasefire over, attacks resumed near the Strait of Hormuz, crude oil jumped nearly 4% to $71.41 — and the VIX fell, dropping to 15.03. Equity markets are treating geopolitical escalation as noise, on the assumption that diplomacy ultimately wins out. Bonds were less relaxed: yields rose almost in parallel across the curve, with the 2-year Treasury at 4.21% and the 10-year at 4.56%, after June Fed minutes revealed some officials arguing for a rate hike. Gold pulled back $57 to $4,120, and the aggregate bond index slipped 0.44%. Economic data was sparse and slightly soft — PMIs, wholesale inventories, and existing home sales all came in a touch below forecasts.

Things We're Watching This Week

1. Tuesday morning, twice. June CPI lands the same morning Chair Warsh delivers his first congressional testimony — and it opens a full inflation gauntlet, with PPI Wednesday and import prices plus retail sales Thursday. After June minutes showed some officials arguing for a rate hike, futures now put roughly 60% odds on one by September. That's the assumption being graded: the market has moved from "when do cuts come" to "how real is the hike talk" in a matter of weeks. A cool CPI likely unwinds the hike pricing; a hot one, with fresh energy costs in the pipeline, hardens it. Either way, Tuesday resets the rate conversation — and with it, bond math for every retirement portfolio.

2. Earnings meet a narrow rally. Last week's gains were carried by very few names — Meta posted its best week since early 2024 on custom AI chip reports, and SK Hynix raised $26.5 billion in the largest U.S. debut by a foreign company. This week the bill comes due: the big banks, TSMC, and ASML all report. When leadership is this concentrated, a small number of earnings reports carry index-level consequences. What we're watching isn't the headline beats — it's whether results give the other 490 stocks a reason to participate.

3. Oil, and the assumption of diplomacy. Crude at $71 with the ceasefire broken is a market saying "this gets resolved." Maybe it does. But note the circularity: a sustained energy spike feeds directly into the inflation prints the Fed is watching, which feed the rate path, which prices every bond and most stocks. Energy risk and rate risk are now the same conversation. The thing that would change our read isn't a headline — it's crude holding above these levels long enough to show up in the August data.

Want the Full Picture?

For the complete index returns, all 11 sector breakdowns, treasury yields, and commodities data, view the full report below.

Read the full weekly data report →

The Bottom Line

For our clients: weeks like the one ahead are why your plan doesn't hinge on any single data print. Whether Tuesday's CPI hardens the hike talk or dissolves it, your income plan, bond positioning, and withdrawal sequence were built to function in both worlds — that's the point of coordination. If the rate conversation raises questions about your own picture, your next review is the place to bring them, or reach out before then.

If you're not yet a client and you're watching a hawkish Fed, $70 oil, and a narrow rally with a retirement date in mind, the right response isn't a prediction — it's a plan that doesn't need one. Our 20-Minute Due-Diligence Conversation is a straightforward way to find out whether your current strategy is built for weeks like this one.