The Oil Collapse Changes the Inflation Math — but Not Enough to Change the Fed's Mind

The Fed held rates steady this week. That was expected. What wasn't expected was how much the meeting clarified what investors are actually worried about — it's no longer about when cuts arrive. The debate has shifted to whether another hike might come first.

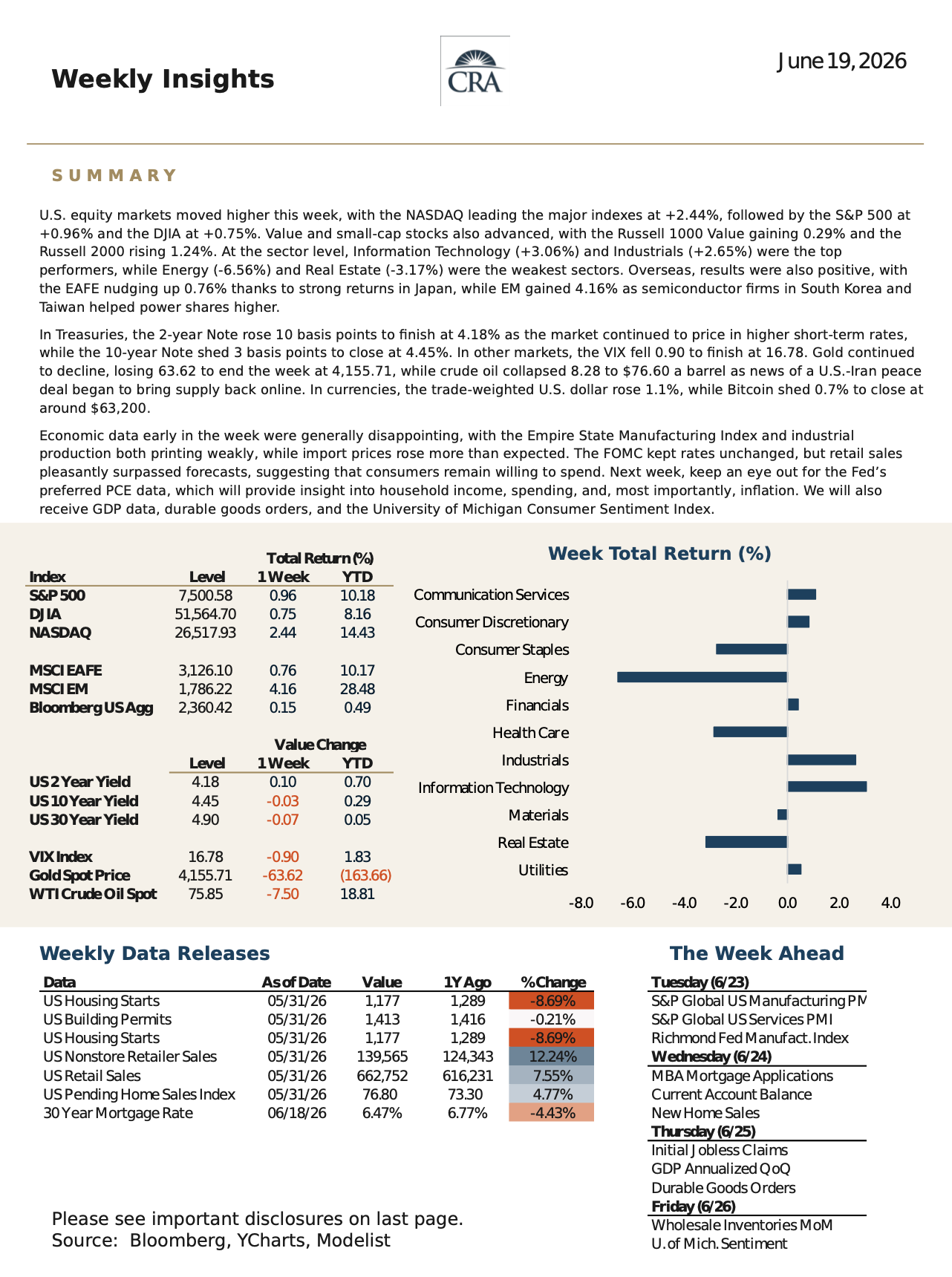

Oil's move last week deserves real attention. Crude shed $8.28 to close at $76.60 a barrel — roughly an 11% decline — after news of a U.S.-Iran peace deal began bringing additional supply back online. That is a meaningful number. Lower energy prices soften the inflation story, relieve pressure on consumer budgets, and give central banks some breathing room. On the surface, it looks like good news.

But the market isn't treating it as a green light, and for good reason.

The problem is what's still in the pipeline. The 2-year Treasury yield rose 10 basis points last week to 4.18%, a signal that markets are pricing in higher short-term rates for longer. Import prices came in above expectations. The Empire State Manufacturing Index and industrial production both printed weakly. And the FOMC's message, while holding the line on current rates, made clear that sticky inflation — not the timing of cuts — is now the central concern. The Fed is watching the same oil move the market is watching. It's not convinced the relief will last, and the Strait of Hormuz remains the variable that could reverse it quickly.

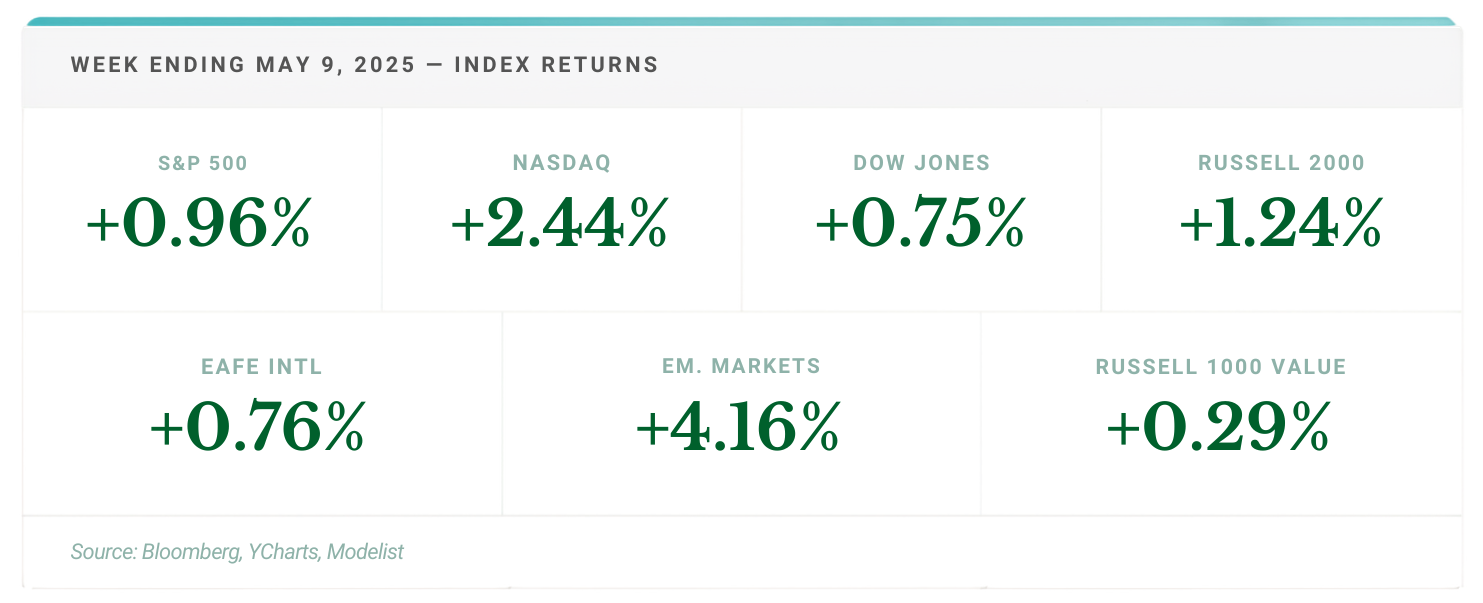

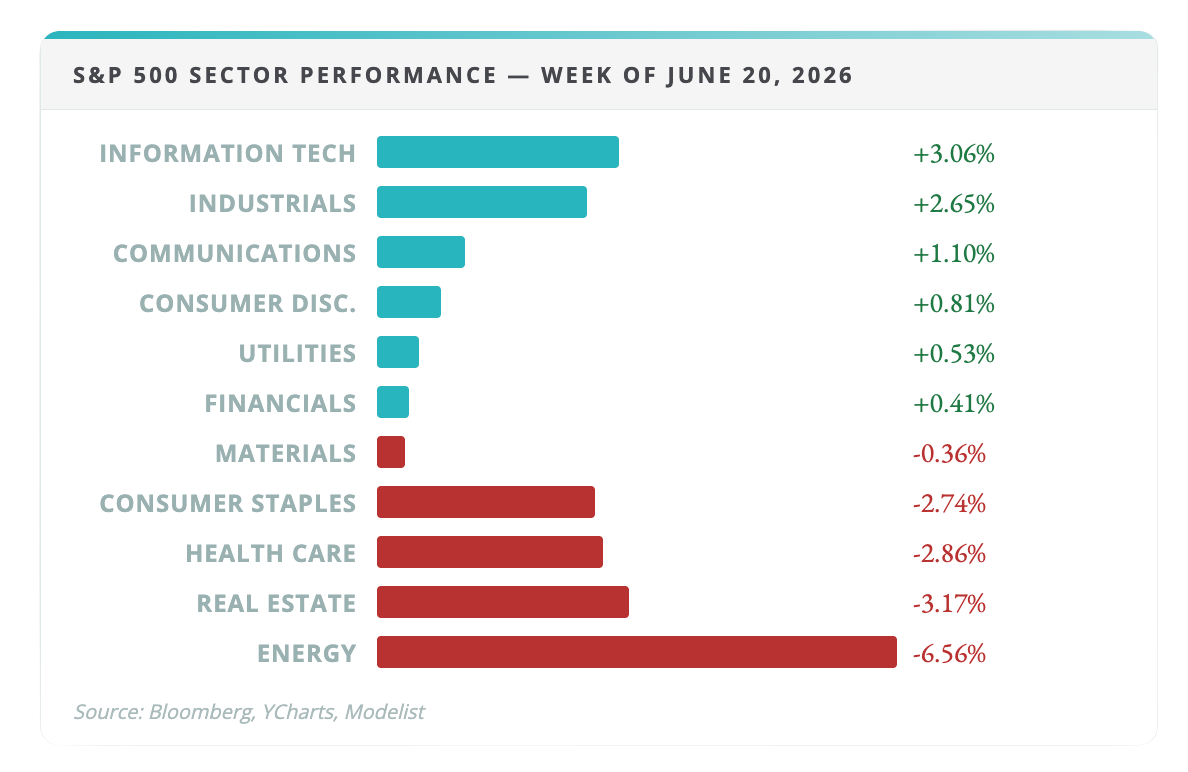

Where the market's optimism showed up most clearly was in Information Technology, which led all sectors with a gain of +3.06%, and in the broader attempt by the rally to widen its base. Small caps rose 1.24%, Industrials gained 2.65%, and Emerging Markets were up 4.16% — powered by semiconductor firms in South Korea and Taiwan. That kind of participation matters. A market where only a handful of mega-cap names are driving gains is fragile. A market where small caps, cyclicals, and international names are joining is structurally healthier. But the question investors are now asking is whether earnings can sustain that broadening — or whether the weight of higher rates eventually pulls leadership back toward quality balance sheets and strong cash flow.

Energy's decline of -6.56% — the steepest sector drop by a wide margin — tells both sides of the story at once. It reflects the oil price relief, which is broadly welcome. It also reflects geopolitical risk that hasn't been resolved, only reduced. Real Estate fell -3.17%, a reminder that longer-duration assets remain under pressure when rate expectations shift even modestly.

Next week brings the data that will tell us whether the Fed's caution was warranted: the PCE inflation reading — the Fed's preferred measure — along with GDP, durable goods orders, and the University of Michigan Consumer Sentiment Index. If PCE comes in hotter than expected, the "higher for longer" trade firms up considerably. If it softens, the broadening rally gets more oxygen.

Want the Full Picture?

For the complete index returns, all 11 sector breakdowns, treasury yields, and commodities data, view the full report below.

View Full Weekly Market Report →

What This Means For Your Retirement Plan

The week's competing signals — oil relief on one hand, sticky inflation and a more hawkish Fed posture on the other — don't require a decision. They require a plan already built for this kind of uncertainty. The Bucket Plan® is designed precisely for moments like this: the short-term bucket isn't exposed to rate pressure, the mid-term bucket doesn't require you to time the broadening rally correctly, and the long-term bucket gives the market time to reward the participation that's now building. The PCE data next week may move markets. What it shouldn't move is your retirement income structure.

If any of this week's news surfaced a question you don't have a clear answer to — about how your income is sourced, whether your plan already accounts for a prolonged high-rate environment, or what a further equity rotation would mean for your withdrawal strategy — that's worth a conversation. The 20-Minute Due-Diligence Q&A Call exists for exactly that kind of specific question.

Schedule a 20-Minute Due-Diligence Q&A Call →