The Rally Is Broadening — But Rates Are the Real Test This Week

Broader participation. A Dow at new highs. Small caps finally showing up. Last week looked like what a healthy rally is supposed to look like — and this week's data will tell us whether it can hold.

The Week in Markets

U.S. equity markets moved broadly higher last week, with the S&P 500 gaining 0.91%, the Dow rising 2.18% to reach a new high, and the NASDAQ advancing 0.48%. Value and small-cap stocks — two areas that have lagged for much of the year — finally participated in a meaningful way, with the Russell 1000 Value up 1.79% and the Russell 2000 rising 2.75%. That kind of breadth is genuinely constructive. When strength spreads beyond a handful of mega-cap names, rallies tend to be more durable.

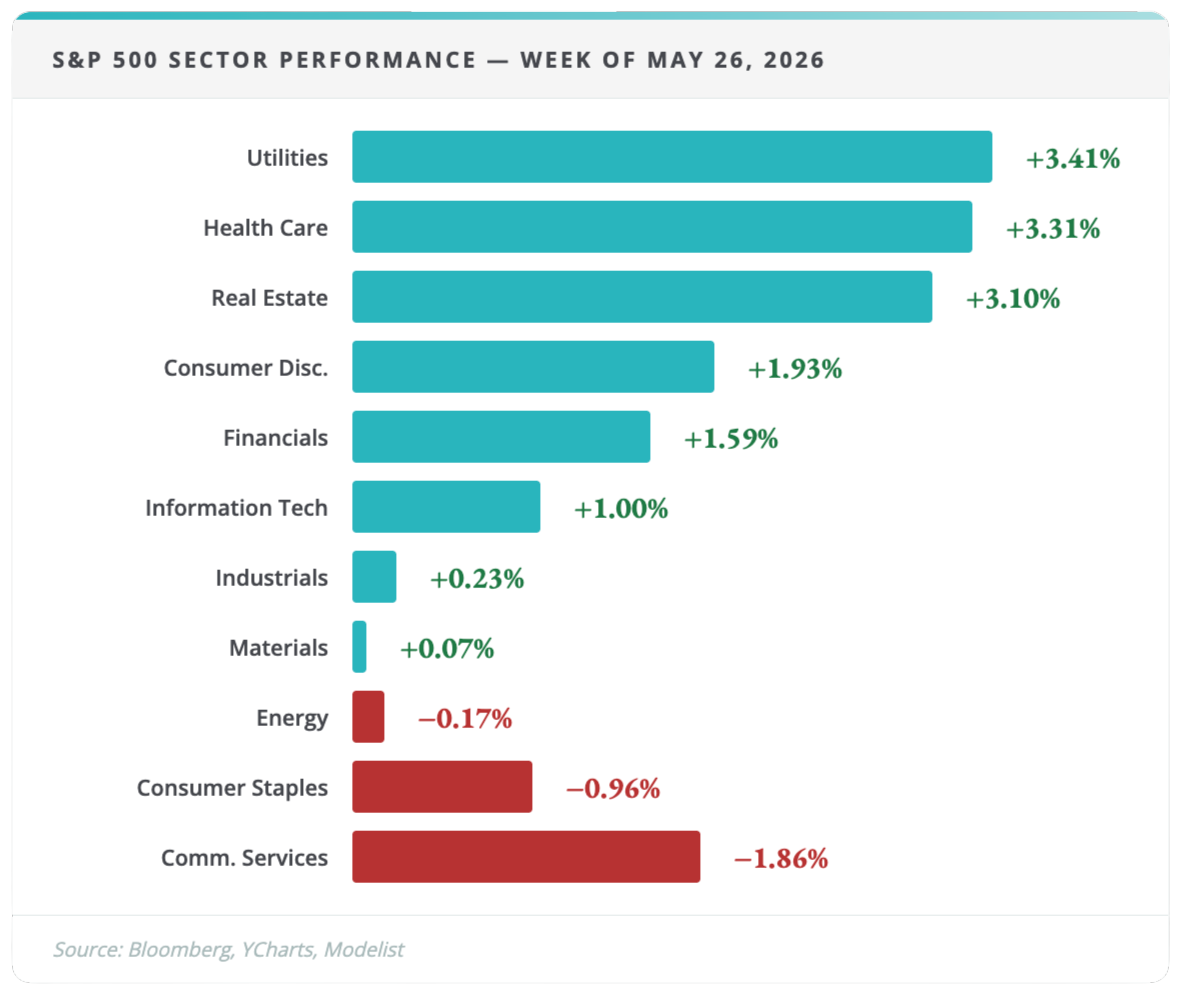

At the sector level, Utilities led all sectors at +3.41%, followed by Health Care at +3.31% and Real Estate at +3.10%. Communication Services was the notable laggard, falling 1.86%, with Consumer Staples down 0.96% and Energy off 0.17%. Overseas, the MSCI EAFE picked up 2.19% behind gains in the U.K. and Germany, while Emerging Markets rose 1.11%, driven largely by Taiwan.

Things We're Watching

1. Breadth Is Back — and That Changes the Conversation

For months, this market's resilience rested on a short list of AI-linked mega-cap names. Last week looked different. Small caps, value stocks, and international markets all moved higher together — the kind of participation pattern that tends to make rallies more durable and less fragile to a single sector reversal. The question heading into this week is whether that broadening has legs, or whether it was a one-week rotation. Earnings season has wound down, so there are fewer catalysts to sustain it from the bottom up. The answer is more likely to come from Friday's economic data than from any individual stock.

2. Friday's PCE Report Is the Number That Matters

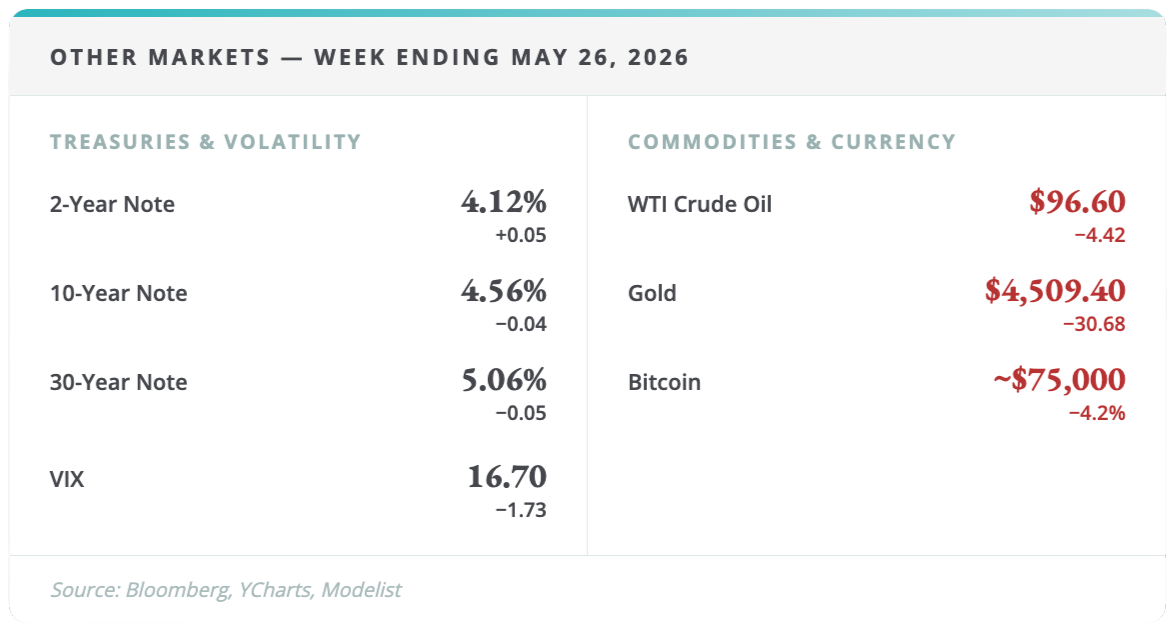

University of Michigan consumer sentiment came in well below forecasts last Friday, with households increasingly worried about inflation — a data point worth taking seriously, since consumer expectations have a way of becoming self-fulfilling. But the number that markets will actually reprice around is this Friday's PCE report, which includes the Fed's preferred inflation gauge alongside GDP, durable goods, and new home sales. A hotter-than-expected reading would likely push yields higher, compress valuations, and extend the timeline on any rate relief. Conference Board consumer confidence also drops this week, and it will either confirm or contradict what Michigan showed Friday. For retirees with income strategies tied to the rate environment, this is the week to watch.

3. The AI Story Is Intact — but the Load Is Getting Heavier

The earnings narrative supporting large-cap technology remains real. Better-than-expected results from major chipmakers and continued strength from mega-cap names confirm that the AI infrastructure buildout is ongoing. But as the rate-cut timeline extends and yields stay elevated, the market is starting to ask harder questions about concentration. If leadership continues to broaden — into energy infrastructure, healthcare, and global supply chains — the rally becomes more durable. If it stays narrow, the underlying risk remains high. Last week's breadth was an encouraging signal. This week's data will determine whether the macro conditions exist to sustain it.

Want the Full Picture?

The full Market Insights report includes multi-period equity and fixed income data, sector detail tables, style box performance, and the complete economic calendar for the week ahead.

View Full Weekly Market Report →

What This Means for Your Retirement Plan

A broadening rally and a Dow at new highs are genuinely good news. But the week ahead — with PCE, GDP, consumer confidence, and new home sales all landing within a few days of each other — means the environment that produced last week's gains is about to be stress-tested. For clients of CRA, none of this requires a reaction. Your income strategy doesn't depend on where the Dow closes Friday. Your Roth conversion math and withdrawal sequencing aren't driven by a single PCE print. The CRAve Life Advisory Process™ is built to hold up through exactly this kind of uncertainty — weeks where the headline and the underlying details are pulling in different directions at once.

For those not yet working with a coordinated plan, this is a useful moment to ask an honest question: if Friday's data comes in hot and rates reprice, do you know what that means for your income, your bond holdings, and your tax exposure — and do you have a structure that accounts for all three simultaneously? If not, the 20-Minute Due-Diligence Q&A Call is where that conversation starts.

Schedule a 20-Minute Due-Diligence Q&A Call →