Weekly Market Insights — Silicon Leads, Sentiment Lags

The Week in Markets

The technology sector carried the tape again this week — while the American household told a different story.

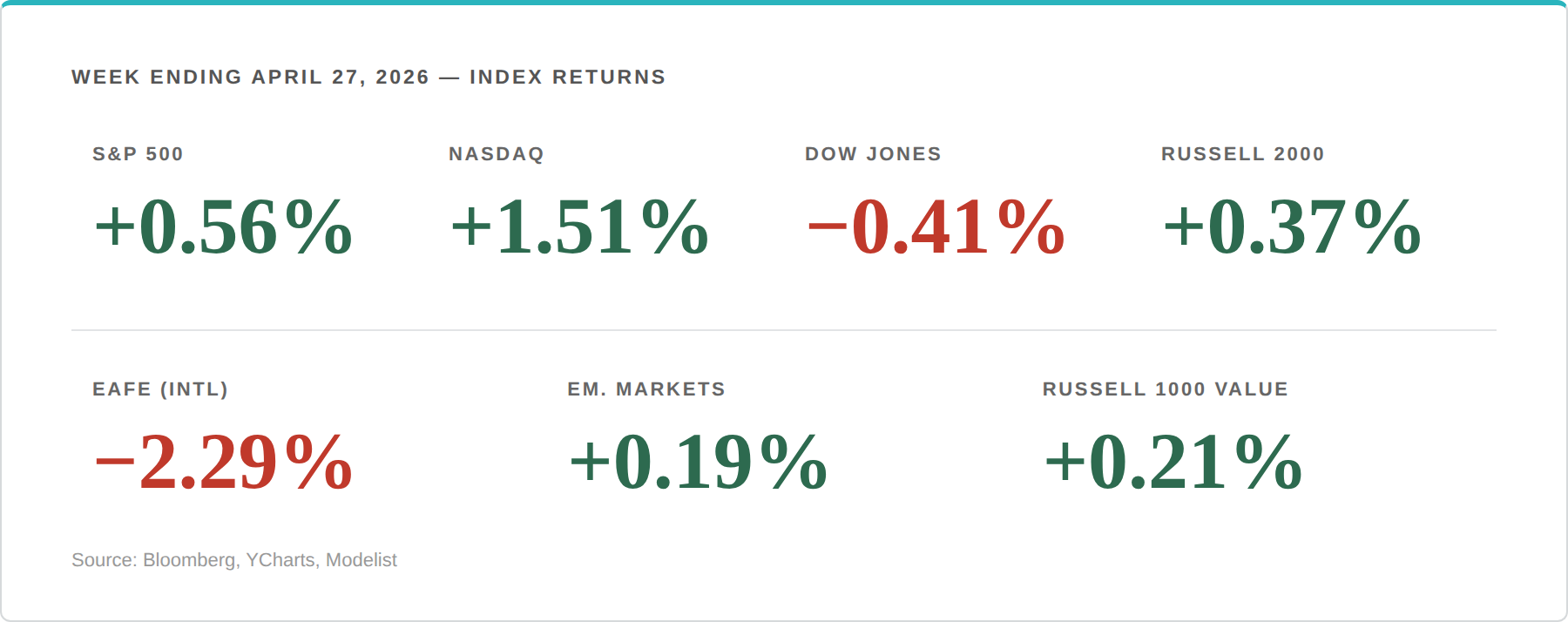

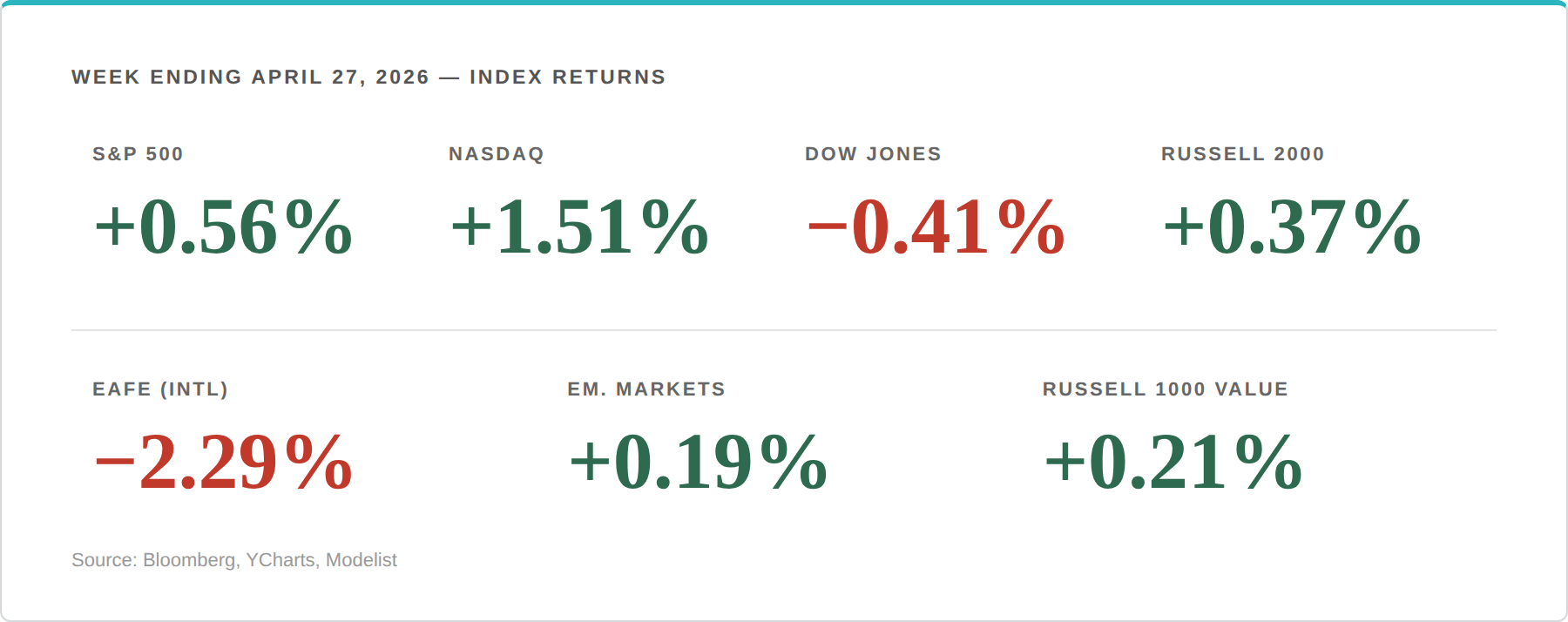

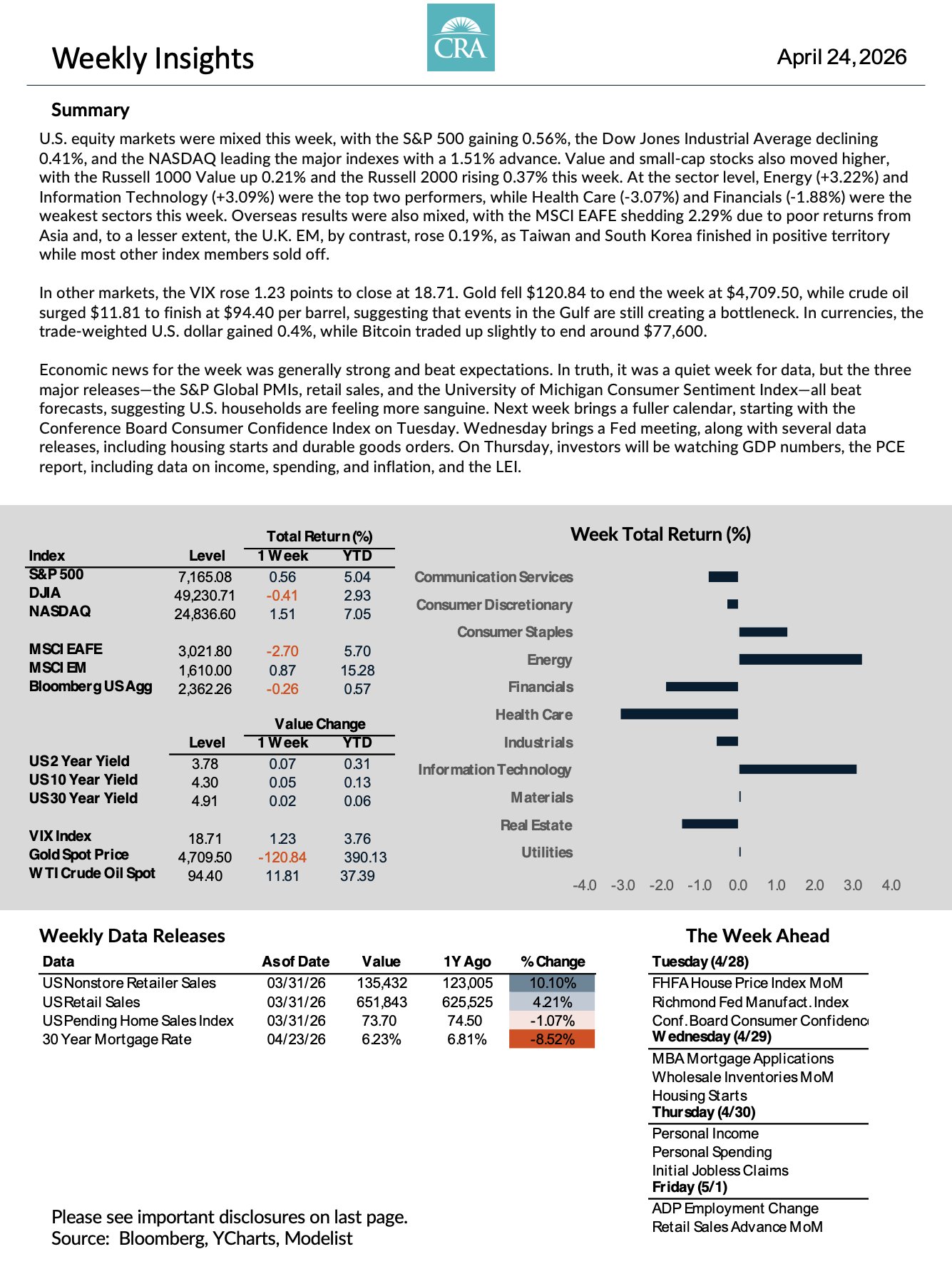

U.S. equity markets finished mixed. The NASDAQ led major indexes with a 1.51% advance, the S&P 500 gained 0.56%, and the Dow Jones Industrial Average slipped 0.41%. Value and small-cap names edged higher alongside — the Russell 1000 Value rose 0.21% and the Russell 2000 gained 0.37%.

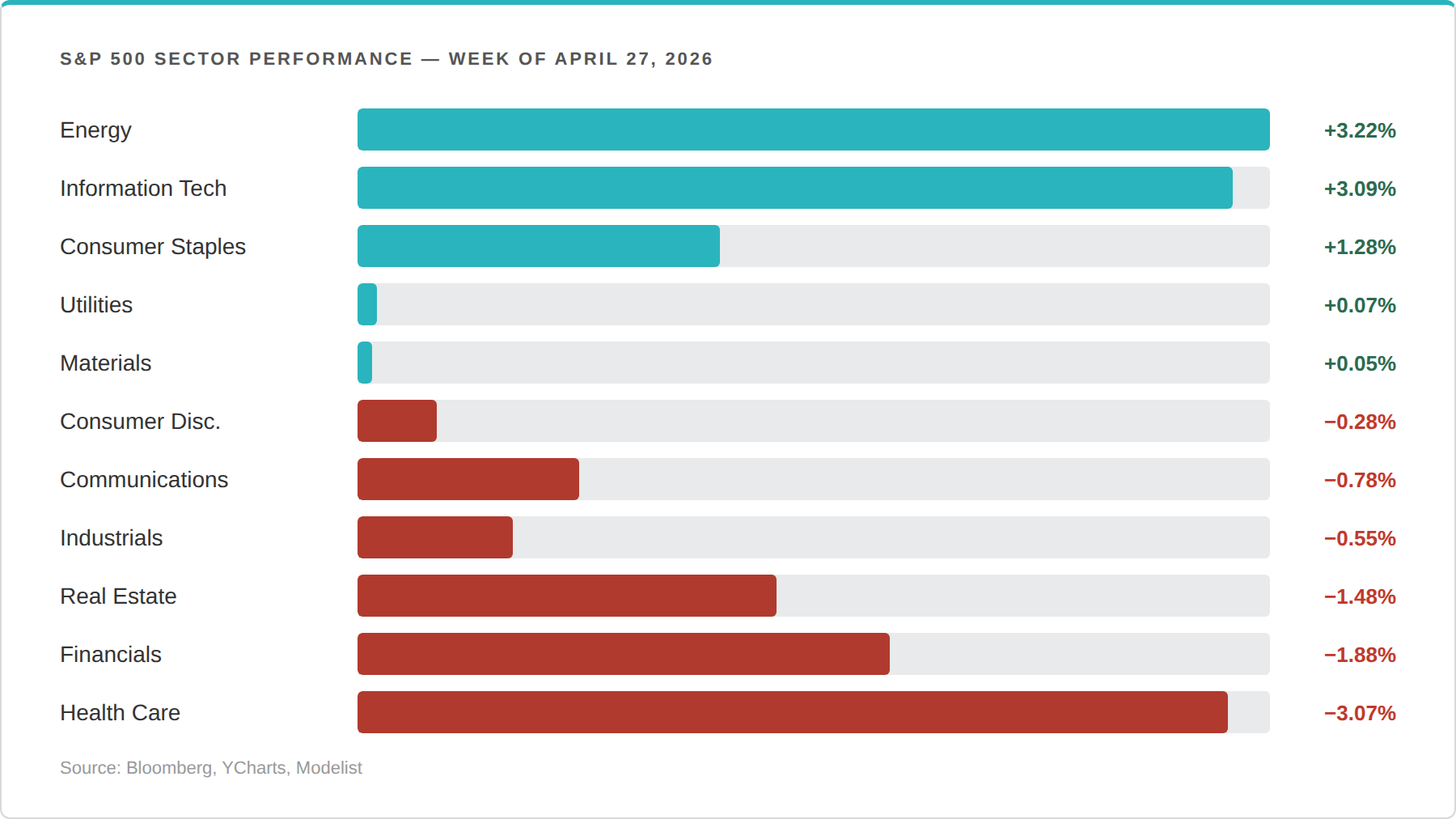

At the sector level, Energy (+3.22%) and Information Technology (+3.09%) were the week's clear leaders. Health Care (-3.07%) and Financials (-1.88%) were the laggards.

International results were mixed. The MSCI EAFE fell 2.70%, pulled lower by weakness in Asia and, to a lesser extent, the U.K. Emerging markets rose 0.87%, as Taiwan and South Korea finished in positive territory while most other index members sold off.

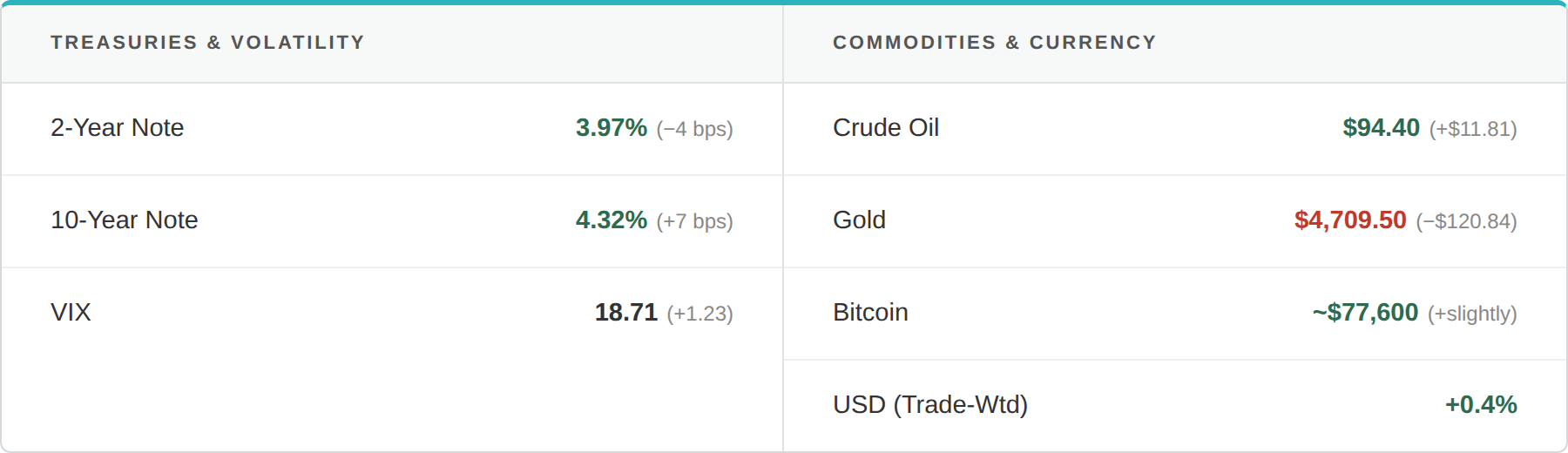

In other markets: the VIX rose 1.23 points to close at 18.71. Gold fell $120.84 to end at $4,709.50. Crude oil surged $11.81 to finish at $94.40 per barrel — a reminder that geopolitical bottlenecks in the Gulf continue to pressure energy supply. The trade-weighted U.S. dollar gained 0.4%. Bitcoin traded up slightly to close around $77,600.

Economic news for the week generally beat expectations. The three major releases — the S&P Global PMIs, retail sales, and the University of Michigan Consumer Sentiment Index — all came in ahead of forecasts.

Things We're Watching This Week

1. Silicon Carries the Tape — and the Echoes of 1999 Are Getting Louder

Intel's blowout earnings drove a roughly 23% one-day move this week, helping extend the iShares Semiconductor ETF's 18-session win streak. Nvidia briefly retook the $5 trillion market cap mark. Strategists are now openly drawing parallels to the late 1990s — a period defined by extraordinary tech enthusiasm, and eventually, a reckoning.

The rally's logic rests on AI capital expenditure continuing to justify the spend. As long as hyperscaler guidance keeps validating the investment cycle, semiconductors remain the market's primary driver. The risk is clear: when that earnings math starts to wobble, leadership will narrow quickly — and it will show up in index returns before most investors have time to reposition.

2. Two Tapes, Two Americas

The S&P 500 and Nasdaq closed at fresh record highs for the fourth consecutive week. At the same time, the University of Michigan's final April consumer sentiment reading printed at 49.8 — the lowest in the survey's history dating back to 1952. That is below both the financial crisis trough and the pandemic low.

This disconnect is not a rounding error. Equity returns right now are concentrated in a narrow band of mega-cap earners. The household experience runs through gas prices and grocery bills — and by that measure, confidence has collapsed.

A rising S&P 500 headline does not mean the broad economy feels healthy to most Americans. These are two different realities running simultaneously.

3. One of the Most Consequential Weeks of the Year Starts Monday

The week of April 28 stacks an unusual number of market-moving events into roughly 96 hours: the Federal Reserve's rate decision, earnings reports from five of the Magnificent Seven, advance Q1 GDP, March PCE inflation data, the ECB decision, and ISM Manufacturing.

Futures currently price a hold at 3.50–3.75%, which means the Fed decision itself is unlikely to be the catalyst. The read will come from Chair Powell's language — how he characterizes the inflation and employment outlook will carry more weight than the rate outcome. Separately, Magnificent Seven names are already up double digits this month. That raises the bar for guidance to surprise to the upside. How companies describe the road ahead may matter more than what they report for Q1.

For investors, positioning into this stretch matters more than the average week.

Want the Full Picture?

The complete Market Commentary report includes detailed index data, fixed income tables, equity performance charts, and the full economic calendar for the week ahead.

What This Means for Your Retirement Plan

Markets can produce four consecutive weeks of record highs and a 73-year low in consumer confidence at the same time — and both can be true simultaneously. For clients of CRA, this kind of environment is exactly what a coordinated plan is built for. Your income strategy is designed to be independent of what the Nasdaq does in any given week. Your tax exposure and withdrawal sequencing are not tied to sentiment readings. The structure is there so that weeks like this one — where the signal is noisy and the headlines point in opposite directions — require no reaction from you.

For those who aren't yet working with a coordinated plan, this week illustrates the core challenge: when markets are concentrated, data is contradictory, and a high-stakes earnings and policy week looms, it is genuinely difficult to know what to hold, what to adjust, and what to leave alone. A 20-Minute Due-Diligence Q&A Call is not a commitment — it is a conversation to understand whether a more coordinated approach would serve your situation.

Schedule a 20-Minute Due-Diligence Q&A Call →