Weekly Market Insights — The Exhale Rally: What Comes Next

The Week in Markets

Call it the exhale rally.

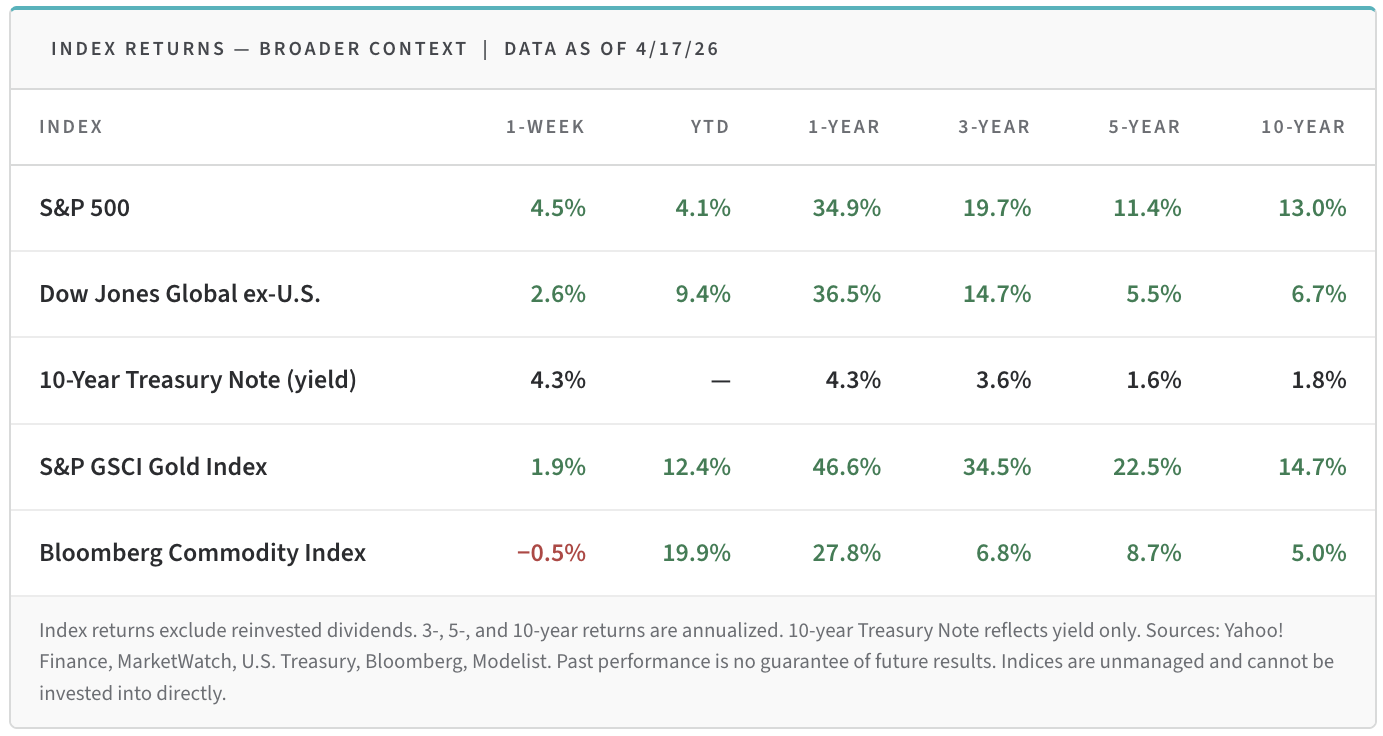

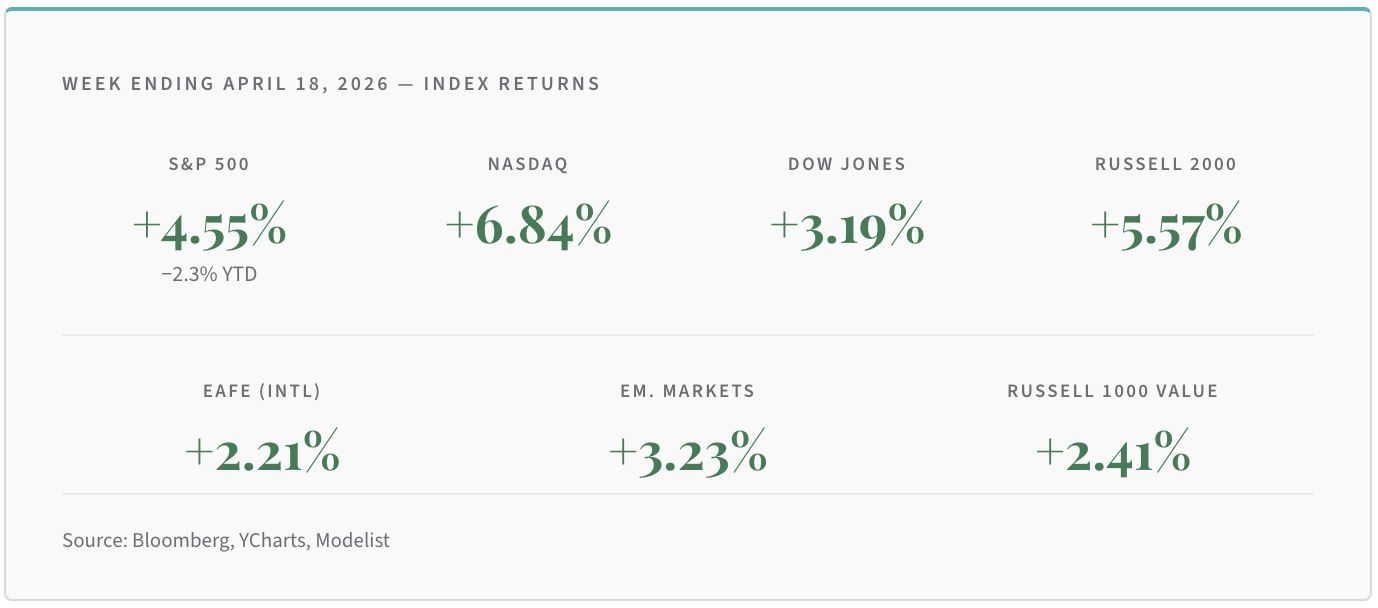

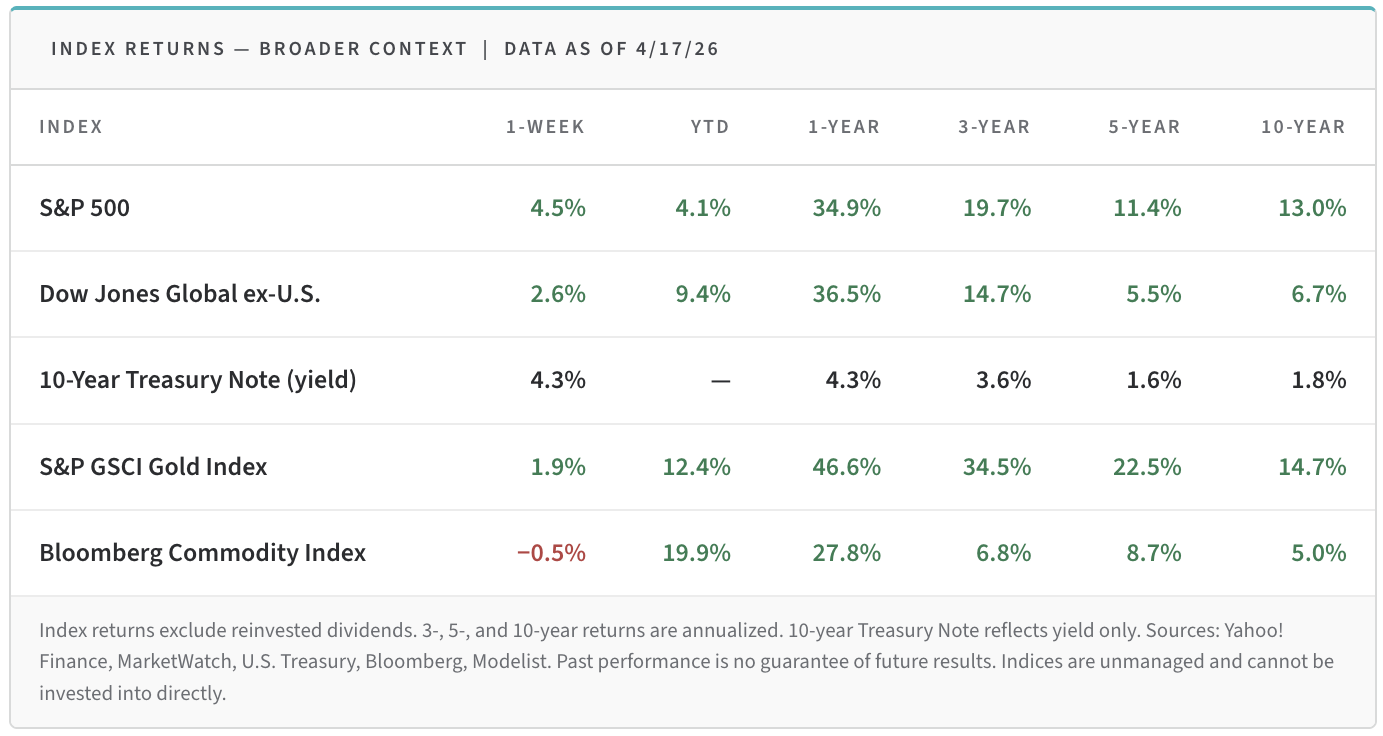

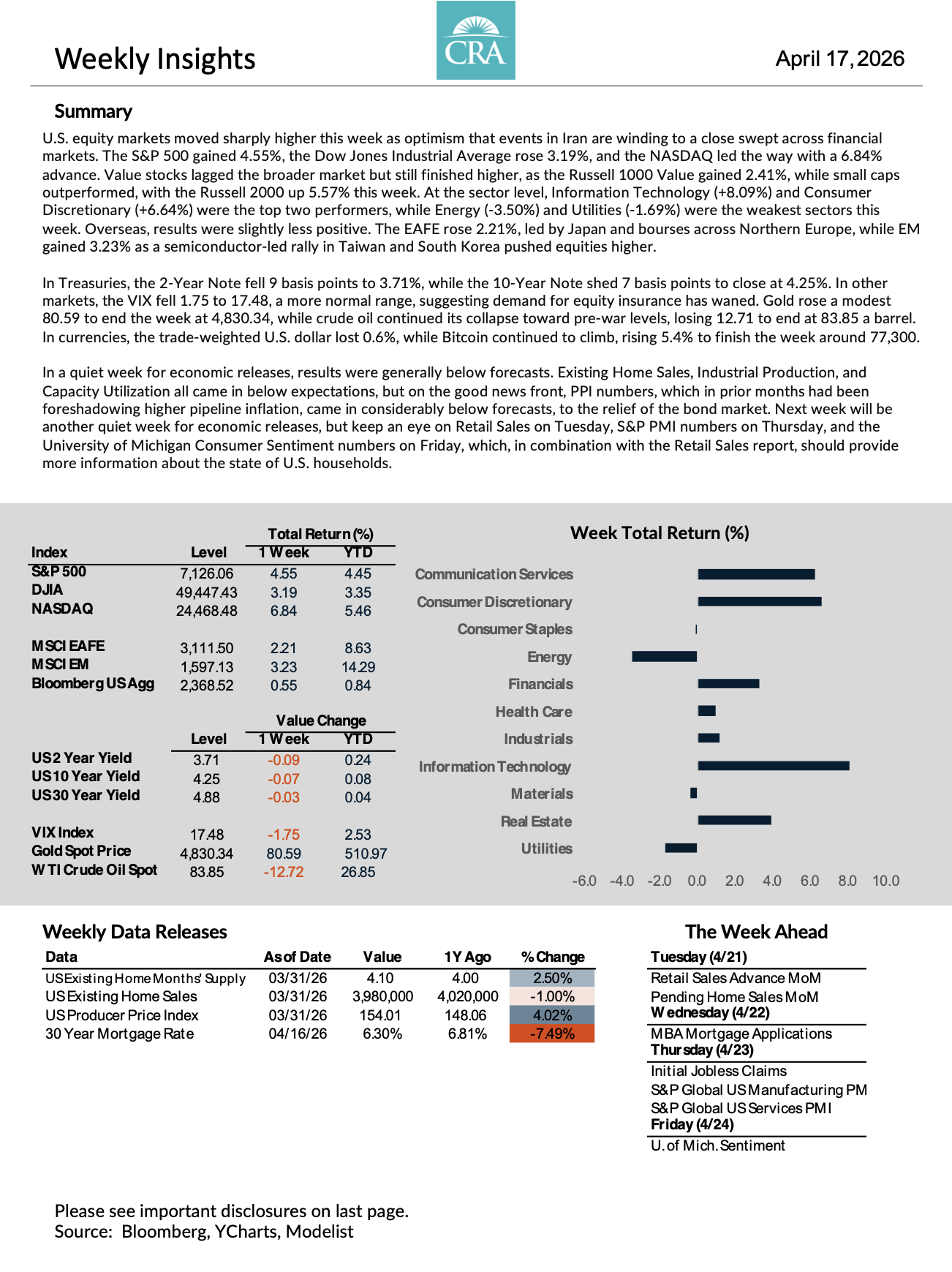

Markets got the news they were waiting for — and they didn't waste a second. The ceasefire that was a question mark heading into last week became reality, and risk assets repriced almost immediately. The S&P 500 gained 4.55% on the week. The NASDAQ surged 6.84% — its 13th consecutive winning session, the longest streak since 1992. Small caps joined in, with the Russell 2000 up 5.57%. Overseas, the EAFE gained 2.21% and Emerging Markets added 3.23%, led by semiconductors in Taiwan and South Korea.

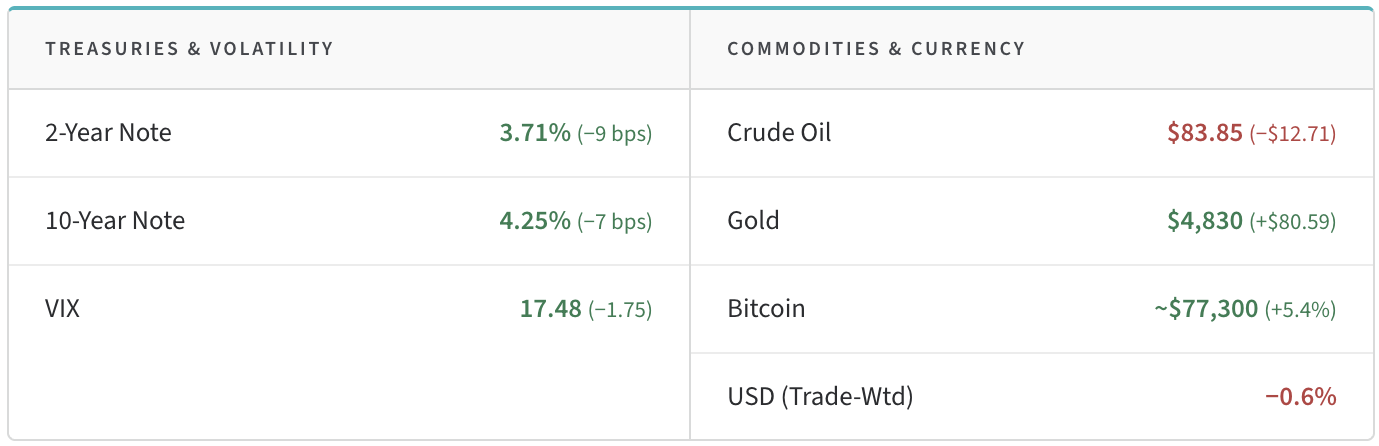

Crude oil told the whole story in one number: down $12.71 to close at $83.85 — the market's clearest signal that the geopolitical risk premium was coming out fast.

Things We're Watching This Week

1. The Oil Reversal Is Real — But It's on a Short Leash

Iran declared the Strait of Hormuz open. A fragile Israel-Lebanon ceasefire held. Crude fell from $113 on April 7 to under $84 this week — and equity, bond, and credit markets all rallied on that single signal. The VIX dropped to 17.48, gold added to $4,830, and the trade-weighted dollar slipped 0.6%. In Treasuries, the 2-Year Note fell to 3.71% and the 10-Year closed at 4.25%.

But the truce is barely 10 days old and oil is still up over 40% year-to-date. The risk premium came out fast — and it can reprice just as quickly. Watch whether inflation expectations stay anchored if any shipping disruptions return. This is relief, not resolution.

2.

Growth Is Back in Front — Earnings Will Decide If It Stays There

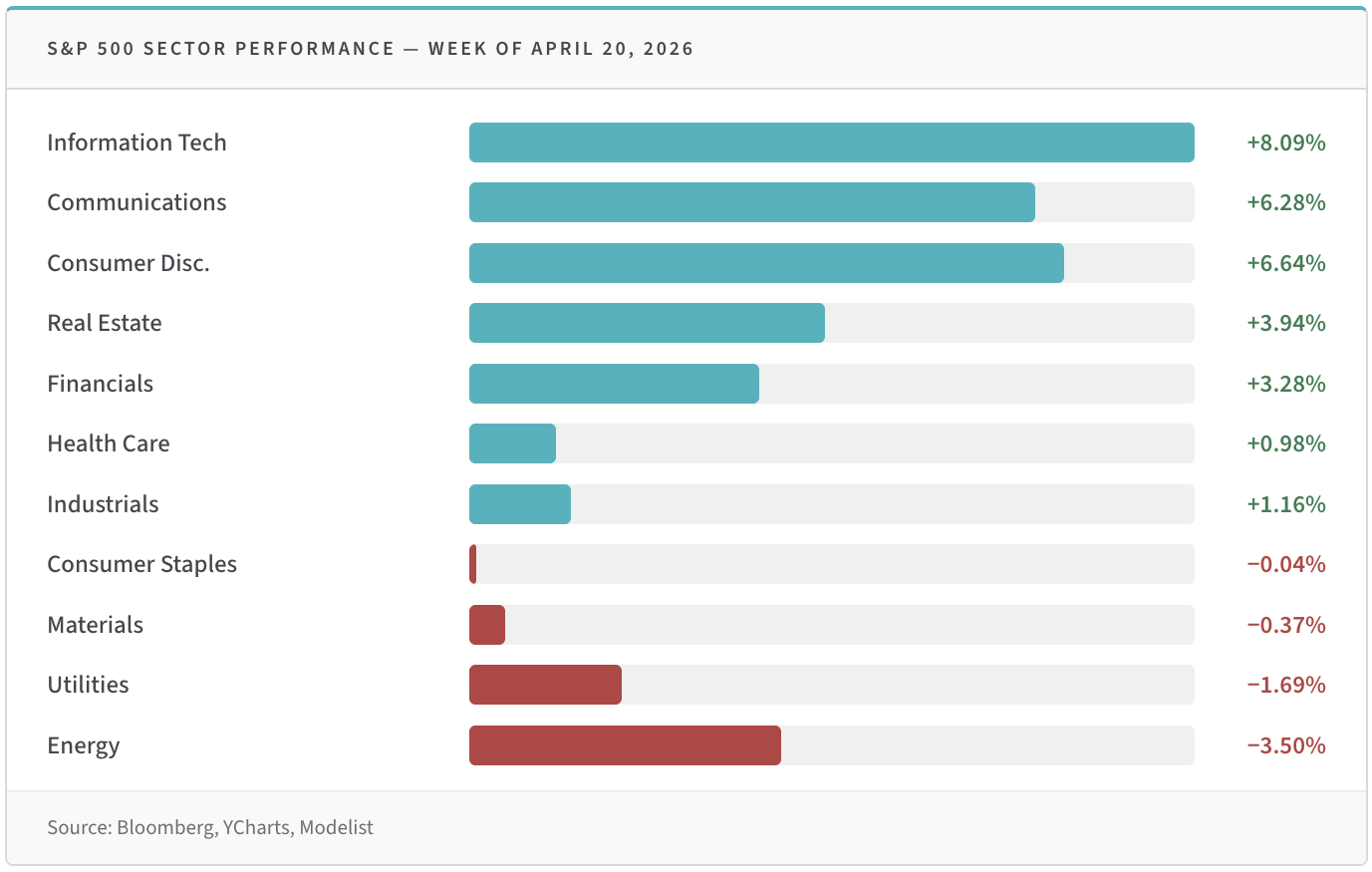

Growth beat value by 430 basis points this week — the third straight week of outperformance. The moment geopolitical fear fades and the rate narrative cooperates, long-duration growth names get bid. Value still leads year-to-date, but the gap is closing fast. The NASDAQ's historic streak is momentum-driven — the question earnings season now has to answer is whether the fundamentals back it up.

3.

Banks Set the Bar High — Now Tech and Industrials Have to Clear It

Financials are tracking 19.7% Q1 earnings growth, up from the 15.1% expected entering the week, with strong trading revenue and constructive consumer commentary doing the heavy lifting. That matters because the S&P's recovery has outpaced estimate revisions — multiples are stretched heading into the next wave of reports.

Tech and industrials report in the coming weeks. If margins hold and guidance stays constructive, the rally has legs. If guidance wobbles, the growth-led rebound gets tested quickly. Tone will matter more than the raw numbers.

Want the Full Picture?

Sector-level data, fixed income detail, top & bottom S&P 500 stocks, and the full economic calendar.

What This Means for Your Retirement Plan

A week like this one feels like confirmation — the fear was overblown, the market recovered, everything is fine. And for one week, it was. But markets recovering and risks being resolved are two different things. The ceasefire is new, oil is still elevated, and consumer sentiment remains near historic lows. Relief rallies are also historically when investors make reactive decisions they later regret — chasing performance, abandoning defensive positions, or mistaking a week for a trend.

For our clients: your income plan, tax strategy, and risk exposure were built for environments like this one — not just the good weeks, but the uncertain ones too. Nothing about this week changes your plan. That's the point.

For those just getting to know us: if you've been navigating this market without a coordinated plan — or working with a team that doesn't connect your investments, taxes, and income strategy together — this is a good time to have that conversation.

Click below to book a 20-minute call to see if what we do is what you need.

Schedule a 20-Minute Call →

"The investor's chief problem — and even his worst enemy — is likely to be himself." — Benjamin Graham