Where are Interest Rates Heading?

The Markets

Was inflation higher, lower, or steady?

Perspective has a tremendous influence on how we perceive the world around us. If you saw any three-dimensional chalk drawings on sidewalks this summer, you understand how perspective affects understanding. When seen from one direction, a chalk drawing looks flat. When seen from another, a winged dragon surges from a hole in the pavement.

Last week, major news sources had varied perspectives on inflation. Here are a few of the headlines we saw:

“Core Inflation Rises to 3.1 [percent]” (Barron’s)

“Inflation holds steady…” (CNN)

“Inflation cools slightly in July from prior month” (Fox Business)

Remarkably, all were correct. The news sources simply highlighted different aspects of the Consumer Price Index (CPI). Here’s what the CPI showed for June and July of this year.

| June 2025 (month to month) | July 2025 (month to month) | June 2025 (year over year) | July 2025 (year over year) |

Headline inflation (all items measured) | 0.3% | 0.2% | 2.7% | 2.7% |

Core inflation (excludes volatile food and energy prices) | 0.2% | 0.3% | 2.9% | 3.1% |

Headline inflation moved slightly lower, on a month-to-month basis (from June to July). It remained steady year over year, which is the 12-month period through July 2025. In contrast, core inflation, which excludes volatile food and energy prices, moved slightly higher on a month-to-month basis (from June to July). It increased year over year.

The Federal Reserve (Fed)’s target for inflation is 2 percent.

The Producer Price Index (PPI) came out last week, too. It tracks how prices have changed for groups that produce and sell goods and services. It was up 3.3 percent in July, year over year, which was higher than June’s 2.4 percent increase.

“U.S. wholesale inflation accelerated in July by the most in three years, suggesting companies are passing along higher import costs related to tariffs. The producer price index increased 0.9 [percent] from a month earlier, the largest advance since consumer inflation peaked in June 2022…,” reported Augusta Saraiva of Bloomberg.

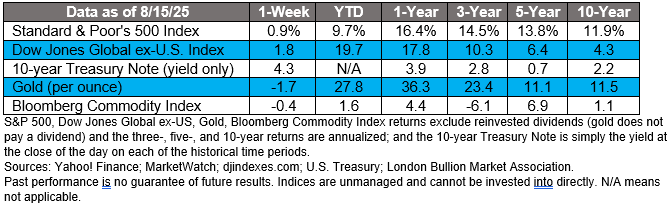

Last week, major U.S. stock indexes continued to rally. U.S. Treasury yields were mixed. Yields for some shorter maturities of Treasuries moved lower, while yields on longer maturities rose.

Where Are Interest Rates Headed?

One of the drivers behind the recent stock market rally has been an expectation that the U.S. Federal Reserve (Fed) will respond to softening economic data by lowering the federal funds rate, reported Saeed Azhar, Johann M Cherian and Sanchayaita Roy of Reuters.

Fed rate cuts are intended to stimulate economic growth by making it less expensive to borrow money. When it’s cheaper to borrow, companies’ expenses may fall and profits can increase, lifting stock prices, reported Mary Hall of Investopedia.

After last week’s Consumer Price Index was released, expectations for a September Fed rate cut soared above 90 percent, according to CME FedWatch. “Inflation is still higher than the Federal Reserve would like — but not high enough to stop the central bank from cutting interest rates next month. That’s investors’ takeaway from yesterday’s consumer price index report,” reported Phil Serafino and Edward Bolingbroke of Bloomberg.

The catch is that a Fed rate cut doesn’t always have the intended effect. Sometimes, the Fed reduces or increases the federal funds rate and other interest rates don’t follow suit. Bloomberg Economics Chief Economist Tom Orlick explained:

“Let’s cast our minds back briefly to the early 2000s, to [former Fed Chair] Ben Bernanke and to the famous savings glut hypothesis. So, back then, the Fed was hiking [the federal funds rate] but long-term Treasury rates weren’t going up. Bernanke said it’s because there’s a glut of global savings. All of this money is coming from China and Saudi into the U.S. Treasury market…that situation is reversed and we’re no longer in a world with a savings glut. We’re in a world with a savings shortage. And that means it doesn’t matter who President Trump appoints as the next Fed chair…that savings shortage is going to mean that long-term rates, the 10-year Treasury yield stays high and…we think 4 to 5 percent for the 10-year Treasury is the new normal.”

The 10-year U.S. Treasury note yielded 4.27 percent at the start of last week. By week’s end it was at 4.33 percent.

Weekly Inspiration

“I don't think there's too much normal out there anymore. Though there's still plenty of average to go around.”

― John David Anderson, Author

Best Regards,

California Retirement Advisors