Who's Happy?

The Markets

Happy holidays!

Over the past year, financial markets reminded all of us that progress is rarely linear. As markets gyrated higher and lower, one truth remained constant – building wealth is the result of diversification, discipline, and thoughtful planning.

An important aspect of planning is the year-end review. If you haven’t yet taken steps to make sure your portfolio is well-positioned for 2026, here are some important things to consider as 2025 comes to a close:

Portfolio drift. The stock market has delivered extraordinary performance. The Standard & Poor’s 500 (S&P) and Nasdaq Composite Indexes are on course to deliver a third year of double-digit returns, reported Elizabeth O’Brien of Barron’s. Strong returns can cause a portfolio to shift from its intended allocation. For example, a portfolio that held 60 percent stocks and 40 percent bonds in 2020 would have drifted from its intended allocation to 76 percent stocks and 24 percent bonds, causing the investor to take more risk than originally intended. A year-end review is a great way to determine whether your portfolio needs to be rebalanced.

Tax savings. There may be steps you can take before year-end to lower your 2025 taxes. The One Big Beautiful Bill Act created new benefits that have income eligibility thresholds, so lowering income could result in a lower tax bill.

One way to lower taxable income is by contributing to tax-deferred retirement plan accounts, such as workplace retirement plans, tax-deferred IRAs, and/or Health Savings Accounts. For example, in 2025, the maximum tax-deferred 401(k) contributions is:

- $23,500 for people younger than 50,

- $31,000 for people 50 and older who make catch-up contributions, and

- $34,750 for 60- to 63-year-olds who make super-catch-up contributions.

Gift giving. There’s another way to reduce taxable income – give a charitable gift. Taxpayers who are 70½ or older can lower their adjusted gross income by taking a qualified charitable distribution, also known as a QCD. They can give up to $108,000 from a traditional IRA directly to a qualifying charity – and the amount counts toward 2025 required minimum distributions, reported Joy Taylor of Kiplinger.

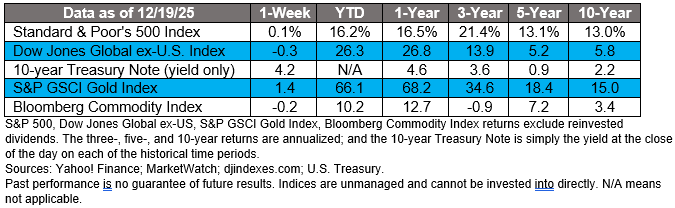

Last week, the Standard and Poor’s 500 and Nasdaq Composite Indexes eked out gains, while the Dow Jones Industrial Average moved lower. Yields on most maturities of U.S. Treasuries moved lower over the week.

Who's Happy?

It’s that time of year – the World Happiness Report (WHR) is here! It evaluated global happiness in 147 countries using surveys of citizens who rate life satisfaction, as well as factors related to economic factors, social support, healthy life expectancy, freedom to make life choices, generosity, and perceptions of corruption. The rankings are based on a three-year average of quality-of-life assessments.

Let’s review the rankings. The countries where people were happiest included:

- Finland (for the 8th consecutive year),

- Denmark,

- Iceland,

- Sweden, and

- Netherlands.

The countries where people were the least happy included:

143. Zimbabwe,

144. Malawi,

145. Lebanon,

146. Sierra Leone, and

147. Afghanistan.

The U.S. dropped to its lowest ever ranking

From 2012 to 2024, the United States dropped from 11th to 24th in the ranking – it’s lowest position ever. The 2024 WHR found that there was a significant difference in happiness by age. Americans age 60 and older were among the happiest in the world for their age group (10th for life satisfaction), while Americans younger than 30 were relatively unhappy (62nd for life satisfaction). The 2025 WHR found that Americans age 30 and younger had the lowest level of social connection and sense of well-being among all U.S. age groups. Interestingly, the report found a strong connection between sharing meals and social connection.

People underestimate the kindness of others

Here's some happier news: In general, people are kinder and more trustworthy than many believe. For example, the “wallet drop” experiment found that “two-thirds of 200 wallets dropped in 20 North American cities [18 in the U.S. and 2 in Canada] were returned, far higher than the author expected, and double that expected by U.S. respondents” when asked whether they thought strangers would return lost wallets.

“Happiness isn’t just about wealth or growth – it’s about trust, connection and knowing people have your back. This year’s report proves we underestimate how kind the world really is. If we want stronger communities and economies, we must invest in what truly matters: each other,” said Jon Clifton, CEO of Gallup, which runs the surveys.

Weekly Inspiration

Barron’s Andy Serwer: “Some people…suggest that gambling is sort of akin to investing. And I want to go back and we’ll talk about some of those other vehicles, but what about this whole notion that gambling and investing are really just the same thing?”

Schwab CEO Rick Wurster: “Well, I think they’re really different and we’ve been trying to get the message out as loudly as we can about the merits of investing and how over time if you are an investor, if you save and you invest over time, your wealth will accumulate. Over a 10-year period [a] balanced strategy of bonds and equities has never gone down and very rarely have equities gone down over a 10-year period. Over a 20-year period equities have never gone down. The reason I go into that is because the payoff to investing is you’re gonna generate wealth over time. It’s a great way to generate wealth. If you compare that to gambling, gambling is a great way to destroy wealth. Less than 5 [percent] of people that sign up for gambling apps take more money out of the gambling app than they put [in].”

–At Barron’s (transcript), December 19, 2025

Best Regards,

California Retirement Advisors