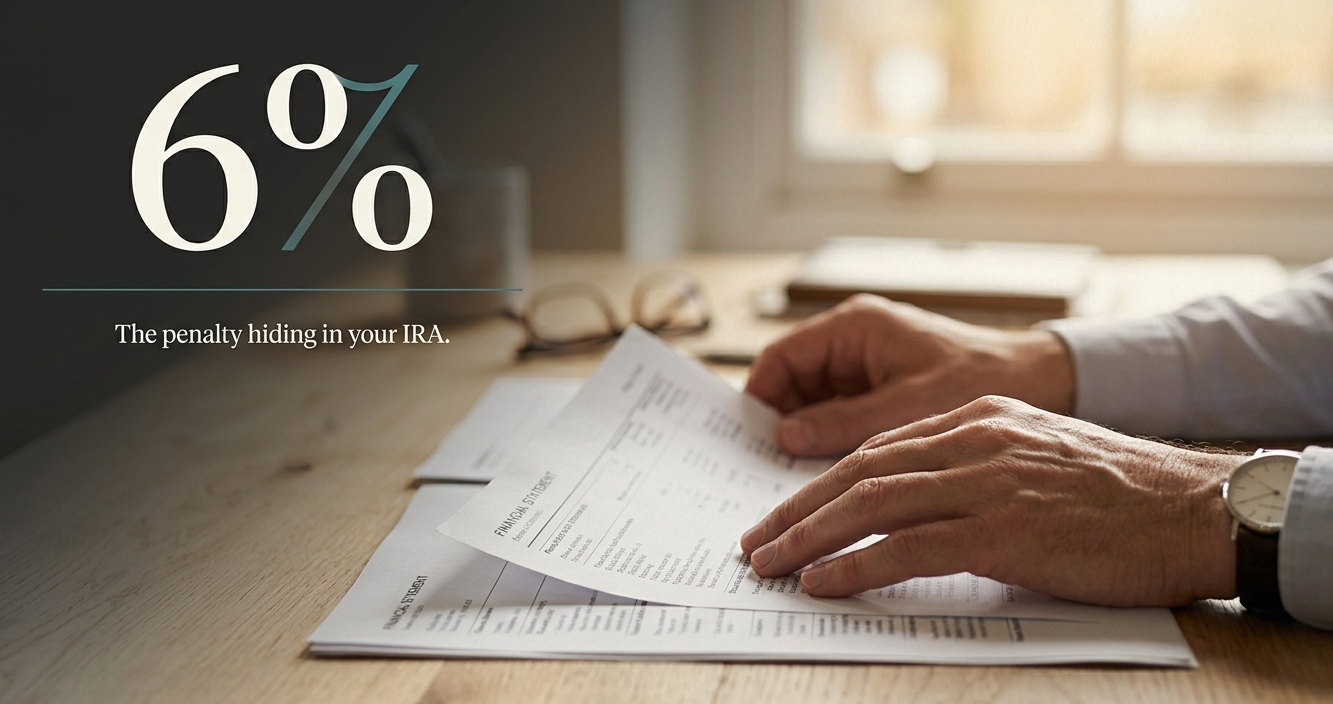

You Didn't Change How You Give. In 2026, the Tax Code Quietly Made Part of It Nondeductible.

A new 0.5% floor now sits under every charitable deduction, and top-bracket donors lost value too. Here's who it hits — and the two moves, including one Wall Street won't mention, that put you back in control.